- Published On: November 13th, 2025Categories: affordable care act, Congress, Democrats, GOP, Medicare, Older Americans, Republicans

As the longest government shutdown in U.S. history finally ends, many of our readers are asking: what does this deal mean for older adults? We supported Democratic efforts to extend Affordable Care Act (ACA) premium subsidies. Without Congressional action to extend these subsidies, millions of “near seniors”— aged 54 to 65— are poised to face dramatically higher health insurance premiums in 2026.

In a statement issued when the Senate deal to end the shutdown was announced, our president and CEO, Max Richtman, warned: “Without those subsidies, ACA premiums could more than double in 2026, forcing people to endure unnecessary financial pain — or lose health coverage altogether.”

Older Americans, who already face higher premiums than younger adults, will have to navigate an even tougher road if these subsidies go by the wayside. “Their lives will be harder, and probably shorter,” says Richtman. “In addition, when those near seniors become eligible for Medicare at age 65, they will be sicker than if they had been able to keep their ACA policies, putting more of a strain on the Medicare program itself.”

As part of the deal to end the shutdown, Senate Democrats have been given a promise that the chamber will vote on a bill to extend the subsidies by the end of the second week of December. Of course, it remains to be seen whether Republicans hold up their end of the bargain. The GOP currently holds a 53-47 majority in the Senate, meaning any successful vote would require at least four GOP defections. Moderates Lisa Murkowski (R-AK), Susan Collins (R-ME), and Thom Tillis (R-NC) along with rural-state populists Josh Hawley (R-MO) and Jerry Moran (R-KS) may be potential ‘yes’ votes to extend the ACA subsidies if it comes to the floor.

Leader Jeffries & Congressional Democrats have not given up on extending ACA subsidies

There is a bit of good news in the shutdown deal for seniors on Medicare. It includes a much-needed extension of Medicare telehealth flexibilities through January 30, 2026, retroactively covering virtual visits from the shutdown period. This will provide critical relief for patients aged 65 and older, who have increasingly relied on telehealth to access care instead of burdensome, in-person doctor visits. Permanent telehealth provisions, such as those for mental health services, are also in effect — and are not impacted by this extension, notes HHS.

The deal also continues extra Medicare payments for hospitals with low patient volumes and disproportionate numbers of senior patients, and will also delay scheduled Medicare payment cuts, including for laboratory tests.

Older Americans’ lives “will be harder, and probably shorter” without ACA subsidies, says NCPSSM president Max Richtman

Unfortunately, the Medicare telehealth coverage extension is only temporary. And, of course, those crucial ACA subsidies remain in limbo for now.

“We must keep fighting to preserve those crucial ACA subsidies so that millions of the most vulnerable Americans don’t lose health coverage.” -Max Richtman, President and CEO, NCPSSM

These next few weeks present a crucial window for the health care status of ‘near seniors.’ It will be especially important for older Americans in red states and districts to make their voices heard, and let their representatives know just how important these premium subsidies are. The shutdown may be ending, but the fight for affordable health care for all Americans continues.

*******************************************************************************************************

Read about relevant policy updates from HHS here

Listen to our podcast here

Find information to contact your representative in congress here

- Published On: November 6th, 2025Categories: affordable care act, Aging Issues, Congress, President Biden, President Trump, Republicans

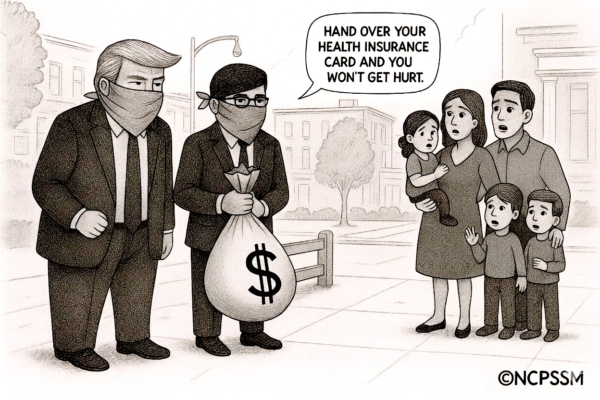

Open enrollment season for Affordable Care Act (ACA) plans arrives amid a severe threat from Trump and congressional Republicans —- who continue to block the extension of crucial ACA premium subsidies. These subsidies have helped middle and lower-income Americans afford health coverage since they were enacted during the Covid pandemic.

This is what the government shutdown — now in its fifth week — is all about. Democrats insist that the subsidies be extended; Trump and the GOP have refused, despite the economic pain and health insecurity their actions will inflict on everyday Americans – including millions of MAGA voters. The president and his party won’t even negotiate with Democrats to end the shutdown.

The consequences couldn’t be more clear. If the subsidies aren’t extended, families with modest incomes will see their ACA premiums double, triple, or even quintuple. Senator Ruben Gallego (D-AZ) shared how premium hikes would affect his constituents. As the Senator posted on X, a family of four in Maricopa County, AZ currently paying $514 per month for an ACA plan will see their monthly premium skyrocket to $2,435 in 2026 without action from Congress.

Senator Ron Wyden (D-OR), ranking Democrat on the Senate Finance Committee, excoriated Trump and Republicans for ignoring the health security of working Americans while showering the wealthy with favors.

“This is about a distorted set of values. They’re giving the tax breaks to the billionaires. Now Trump and the Republicans have decided to try to raise additional revenue for the insurance companies,” said Sen. Wyden on our podcast this week. “They’re using the shutdown as an ‘out’ from paying those subsidies.” – Senator Ron Wyden

Senator Ron Wyden: Trump & GOP values are “distorted”

Our senior health care policy expert, Anne Montgomery, points out that ‘near seniors’ (aged 54-65) will be hit hardest if the ACA subsidies disappear:

“It’s important to remember that many people in their 50s and early 60s are on fixed incomes, but not yet eligible for Medicare. As older folks, they already pay the highest premiums. We’re talking about thousands of dollars more out of pocket, just to keep basic health insurance. It’s an impossible choice: lose coverage, cut back on care, or take a huge financial hit.” – Anne Montgomery, NCPSSM senior health policy expert

A recent analysis from Kaiser Family Foundation demonstrates the hard reality:

-

-

A 60-year-old earning $62,700 (just above the threshold for subsidies if enhancements aren’t extended) would pay nearly $9,600 more per year in premiums.

-

A 64-year-old with that income might have to pay around $11,000 more annually.

-

Even 50-year-olds earning the same amount will pay $4,500 more per year if enhancements end.

-

Middle-income early retirees will especially feel the squeeze as the income threshold for premium assistance is set to drop back to 400% of the federal poverty level, reinstating the old “subsidy cliff.”

It’s also important to remember that President Biden’s Inflation Reduction Act (IRA) enabled more Americans to receive subsidies regardless of income. Currently, eligible households don’t pay more than 8.5% of their income for a benchmark silver plan while after-subsidy premiums could be as low as $10/month. That goes away if Trump and the GOP have their way.

Thanks to these improvements from the IRA, we saw marketplace enrollment hit a record 24.3 million. Without them, the Congressional Budget Office (CBO) projects ACA enrollment could drop by up to 4 million, dramatically increasing America’s uninsured rate.

“If you’re 50–64 and relying on ACA Marketplace coverage, this could be a pivotal year. Be prepared for premium increases and the return of the ‘subsidy cliff’ if Congress does not act. It’s important to shop for plans carefully and monitor policy changes as they happen.” – Anne Montgomery, NCPSSM

Zooming-out from the subsidy battle for a moment, it’s become increasingly obvious that Trump and the GOP are using the shutdown as a smoke screen for larger plans to cut social programs across the board, as part of an effort to destroy the safety net put in place during the New Deal and Great Society. NCPSSM urges Americans to protect themselves by speaking up and speaking out. Contact the White House and your elected representatives and tell them: no more breaks for billionaires, especially at the expense of working people struggling to afford basics like food and health care.

****************************************************

Listen to our podcast with Senator Ron Wyden, here.

Learn more about the ACA Marketplace here.

Read an informative analysis from Kaiser Family Foundation on the consequences of premium increases here.

Related Posts

-

- Published On: October 30th, 2025Categories: Social Security, Social Security Disability Insurance

Shutterstock

Conservative think tanks have been pushing a false narrative that older Americans who collect Social Security are somehow ‘ripping off’ younger adults. This propaganda ignores the facts — pitting hardworking Americans (of all ages) against one another.

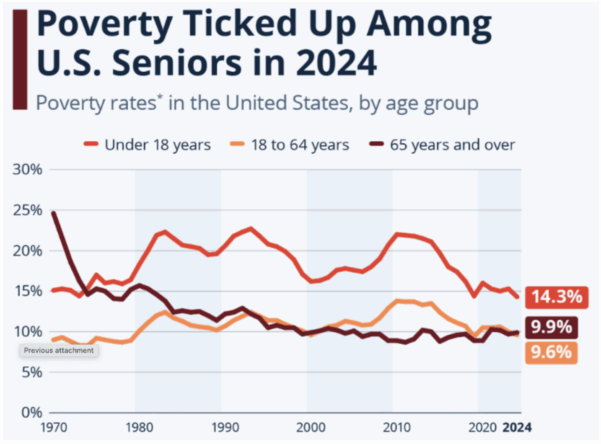

While right-leaning analysts argue that younger workers shouldn’t have to pay into Social Security while wealthy ‘greedy geezers’ collect benefits, the data tells a different story. New statistics show that poverty among seniors is on the rise, reaching 15% in 2024, according to the U.S. Census Bureau’s Supplemental Poverty Measure (SPM).

Seniors now have the highest poverty rate of any demographic group. They also are the only group whose poverty rate increased last year, as pandemic relief programs faded and persistent inflation—exacerbated by Trump’s tariffs—put an additional strain on their finances.

The latest U.S. Census Bureau data shows that seniors continue to face significant economic challenges. Traditional poverty rates (different from the SPM) among Americans aged 65 and older ticked up in 2024, rising to nearly 10%. This contrasts with declines in poverty observed for children and working-age adults during the same period.

Source: Statista, using U.S. Census Bureau data

Experts like Ramsey Alwin of the National Council on Aging warn that Trump/Republican economic policies favoring the wealthy have had a widespread impact on the well-being of American seniors:

“When we lifted up individuals and families during the pandemic, poverty among older Americans went down to 9.5%. When that help went away, poverty increased. Programs like SNAP, Medicare Savings Programs, and Medicaid provide much-needed assistance that must continue. But the recently enacted cuts to SNAP will increase hunger among older Americans and the recently passed Medicaid cuts will lead to a sicker older population.” – Ramsey Alwin, President, National Council on Aging

Social Security and Medicare are lifelines for tens of millions of seniors, many of whom are struggling to make ends meet. The myth that the most vulnerable among us are lining their pockets at the expense of younger generations would be laughable if it wasn’t so harmful.

In a recent piece in Newsweek, NCPSSM President and CEO Max Richtman called Social Security a “win-win for the older and younger generations” and criticized what he called “a false narrative that needlessly pits the generations against each other.”

In fact, younger generations will depend on Social Security even more than today’s seniors. Millennials and Gen Z are less likely to have access to traditional pensions, face record student debt, and have seen housing and healthcare costs rise much faster than wages. Meanwhile, Social Security is there for younger adults now — in the form of life and disability insurance for eligible workers. Millions of younger adults received Social Security survivor benefits as children, after the death or disability of a working parent.

The ‘greedy geezer’ myth has become demonstrably even more false during the second Trump administration, despite the president’s hollow promises to protect Social Security. The administration recently proposed deep cuts to Social Security Disability Insurance (SSDI). These changes would reduce eligibility for SSDI, hitting older workers with disabilities hardest. Advocates warn this could push hundreds of thousands of older Americans into poverty and ill health. Meanwhile, the White House continues to shrink staffing at the Social Security Administration (SSA), resulting in longer wait times and reduced service.

There is no doubt that younger workers face significant financial challenges of their own — and policymakers should address those challenges. But we must continue to call out right-wing propaganda that attempts to undermine Social Security by dividing the generations.

“If conservatives are so concerned about younger adults, why don’t they prioritize spending in ways that would help them — such as housing, affordable medical coverage, and lower-cost college education?” asks Max Richtman. “And why does Social Security need to be sacrificed, when there are other big ticket items that could be scrutinized, including trillions of dollars in tax cuts for the wealthy?”

**************************************************************************Read the latest data about senior poverty here.

Read more about common Social Security “myths” here

Related Posts

- Published On: October 23rd, 2025Categories: Alzheimer's

In this week’s episode of our You Earned This podcast, Dr. Heather Snyder of the Alzheimer’s Association tells us some common misconceptions about Alzheimer’s disease while also sharing exciting developments in research, treatment, and prevention. These advances should be welcome news to America’s seniors, demonstrating important steps forward in the ongoing fight against Alzheimer’s.

Evaluating Data Beyond Anecdotes

Alzheimer’s affects more than 7 million Americans, with nearly 12 million caregivers supporting loved ones who live with the disease. Many people understand Alzheimer’s through the lens of personal experience — family or friends who gradually lost memory and independence. Dr. Snyder emphasized that while those experiences are painful and real, the latest research offers some hope.

“People often think there’s nothing you can do about it… but what we’re learning is that’s changing.” – Dr. Heather Snyder, Alzheimer’s Association

Scientists are identifying tools to diagnose the disease earlier, understand who’s most at risk, and slow cognitive decline with targeted interventions.

Alzheimer’s vs. Dementia

Dr. Snyder says that many people use “Alzheimer’s” and “dementia” interchangeably, but they’re not the same. “Dementia is an umbrella term describing symptoms like memory loss, language problems, and confusion severe enough to affect daily life. Alzheimer’s disease is one of several causes of dementia, along with Lewy body disease, vascular dementia, and others.”

Risk Factors and Genetics

Dr. Snyder noted that age is the strongest risk factor, but says that “aging itself is not the cause.” Other influences include cardiovascular health, metabolic issues, sleep quality, and head injury. Genetics also plays a role, especially a gene known as APOE4, which can increase a person’s risk of developing Alzheimer’s but doesn’t determine it. As Dr. Snyder explained, many people with two APOE4 copies (one from each parent) maintain healthy cognition “into their late nineties,” showing that lifestyle and overall health can affect whether the gene is activated.

“One in nine individuals over the age of 65 has Alzheimer’s or another form of Dementia.” – Dr. Heather Snyder

Dr. Heather Snyder of the Alzheimer’s Association

Dr. Snyder and her colleagues at the Alzheimer’s Association are at the forefront of cutting-edge research exploring how diet, exercise, and other lifestyle modifications may play a vital role in reducing cognitive decline. In a study known as the U.S. POINTER trial, researchers tracked more than 2,000 adults at risk of cognitive decline. Data from a study group that underwent a structured program of modifications —which combined exercise, a nutritious diet, and heart monitoring—showed promise for preserving brain health.

Participants maintained brain function equivalent to being “one to two years younger,” says Dr. Snyder, according to study results published in the Journal for American Medical Association (JAMA). POINTER is the first large-scale U.S. study proving that structured lifestyle changes might actively protect brain health and slow age-related decline.

Meanwhile, NPR reports that playing brain games may improve cognitive function. According to a new study, doing “rigorous mental exercises” for 30 minutes a day increases levels of the chemical messenger acetylcholine in a brain area involved in attention and memory. “The study comes amid a proliferation of online brain-training programs, including Lumosity, Elevate, Peak, CogniFit and BrainHQ,” says NPR.

New Blood Test Offers Earlier Detection

Dr. Snyder is hopeful about recent developments in blood testing to detect Alzheimer’s. Earlier this spring, the FDA cleared the first blood test designed to aid in diagnosis. The blood test offers a less invasive, more widely available method to support accurate and earlier diagnosis, which is crucial for timely intervention and better management of the disease.

“It is a very exciting time as we’re seeing all of this work in the research space translate into the clinical setting. And we’ll see this go even further as we move to primary care and other types of care settings as well for individuals.” – Dr. Heather Snyder

The First Disease-Modifying Treatments

Two medications—Leqembi (lecanemab) and Kisunla (donanemab)—have ushered in the first wave of disease-modifying Alzheimer’s treatments. Both drugs target beta-amyloids, helping clear harmful protein buildup from the brain and slow cognitive decline in early-stage patients.

Medicare covers these drugs under Part B (reimbursing about 80% of their cost once patients meet their deductible) — with the requirement that recipients participate in a data registry tracking real-world effectiveness. In August 2025, the FDA approved a subcutaneous, at-home version of Leqembi, reducing the need for frequent infusions. Kisunla’s monthly infusion model is also designed for shorter treatment duration. Both remain under long-term study to determine sustained benefits.

“Every new study is building on the last. We’re learning from every trial, and each one brings us closer to changing the trajectory of the disease.” – Dr. Heather Snyder

While there’s still no cure for Alzheimer’s, the combined progress in detection, prevention, and treatment points the way toward a potentially brighter future.

**********************************************************

To listen to the full podcast with Dr. Heather Snyder, listen here

Read the Alzheimer’s Association’s FY2024 Annual Report here

For reliable information, resources, and community support, the Alzheimer’s Association offers a 24-hour helpline.

- Published On: October 17th, 2025Categories: Medicare, Medicare Advantage

This year’s Medicare open enrollment season, which began on October 15, comes at a concerning time for the program. There are several crosswinds buffeting Medicare right now, including a government shutdown — and reckless Trump administration cuts at the Centers for Medicare and Medicaid Services. Add to that the increasing dysfunction in the privatized Medicare Advantage program, and you have a higher stakes enrollment season for seniors. We asked our senior health policy expert, Anne Montgomery, to answer some commonsense questions about enrolling in Medicare at this potentially fraught and confusing moment.

Q: Who needs to participate in Medicare open enrollment? Everyone on Medicare?

ANNE: Yes, everyone on Medicare. Whether they are entering the program (turning 65) or have been in it for some time, everyone should examine their options. If someone has already made a choice, they don’t have to change, but it’s always wise to look around and see what’s available. Medicare Advantage (also known as MA or Medicare Part C) is becoming increasingly dominant, with substantial marketing behind it as well. It’s important to understand that open enrollment runs through December. Do your homework: look at providers, drug coverage, and whether your medications are on the formulary. There are many things to check.

Q: What are the most important things for beneficiaries to do or look at this open enrollment season?

ANNE: This is a complicated season, made more so by the ongoing government shutdown. Thankfully, benefits and provider payments are not affected, but parts of Medicare’s administration are running on fumes. If you call 1‑800‑MEDICARE, you may not be able to get through right now, so it’s harder to get good information during a shutdown. The best option right now is to contact your State Health Insurance Assistance Program (SHIP). You can make appointments by phone or in person to sit down with someone who can answer your questions. In my opinion, this is the best way to get informed and explore your options.

Q: We are skeptical of Medicare Advantage as a choice for seniors, given the disadvantages we’ve noted over the years. What should people be cautious about when considering Medicare Advantage?

ANNE: Medicare Advantage plans can look attractive because they make enrollment easy with bundled coverage—you don’t need to think separately about Parts A, B, and D. Many Medicare Advantage plans are like HMOs with limited networks of providers and prior authorizations for care. If you need expensive treatments for cardiac issues or chronic disease, MA plans are notorious for delaying or denying payment for costly services and medications. Beneficiaries can be left financially and legally vulnerable. The appeals process is stressful and sometimes requires legal assistance, which is an added burden.

Q: This year we’ve seen major Medicare Advantage insurers pull out of the market or scale back services. Should this be a concern when choosing a plan?

ANNE: Yes, absolutely. If you sign up for a plan and it later withdraws from your region—these are, after all, for-profit enterprises—you may have to switch mid-course, which is especially difficult during active treatment. This is why personalized, unbiased counseling is crucial. Remember, Medicare Advantage brokers operate under financial incentives, while SHIP staff provide neutral guidance.

Q: The Washington Post reports that a new Trump administration directory designed to help seniors compare Medicare Advantage providers is riddled with errors. How should enrollees handle that?

ANNE: I haven’t tried it myself, but it’s meant to help people identify providers in a simple, comprehensive way. Unfortunately, it has glitches and isn’t yet the reliable resource it was promised to be. That doesn’t mean it can’t improve over time. But for now, it’s a flawed tool and not a complete solution.

Q: Many people are trying to switch out of Medicare Advantage during open enrollment. What obstacles might they face returning to traditional Medicare?

ANNE: There isn’t a structural obstacle, per se. You can still dis-enroll… and many people do after realizing the disadvantages of Medicare Advantage. However, if you return to traditional Medicare and want to buy a Medigap supplemental insurance policy to help with deductibles and co-pays,you may need medical underwriting if you’re more than five months past your 65th birthday. That means if you have pre-existing conditions, your monthly premiums could be significantly higher—or you may be denied a Medigap policy altogether.

Q: How concerned should we be about the Trump administration’s changes to traditional Medicare, such as using AI bots for prior authorizations?

Answer: It’s an interesting development. Prior Authorization has long existed in Medicare Advantage through administrative contractors who are brought in to flag potential overuse by providers. The concern is that AI‑driven prior authorizations in traditional Medicare—run by organizations whose motives aren’t fully clear—might be used in the same restrictive way. That hasn’t happened yet, but if it does, it could harm beneficiaries. All in all, we’d rather have human beings making decisions about our healthcare instead of bots.

Q: The Trump administration has reduced staff at the Centers for Medicare and Medicaid Services. Is that affecting Medicare’s administration?

Answer: It’s difficult to say definitively, but we’re seeing longer wait times and reduced availability for public-facing services like 1‑800‑MEDICARE. Layoffs and budget cuts weaken administrative support, and the problem will grow if these agencies continue being targeted. This pattern extends beyond Medicare. We are seeing it at the Social Security Administration, the Department of Education, HUD, and even air traffic control. Wantonly cutting staff in this way has serious consequences.

Q: Has the government shutdown had any direct effects on Medicare?

ANNE: The hotline is slower, but still functional. It’s taking longer for people to get appointments or resolve administrative issues, and the strain increases the longer the shutdown continues. The good news is that no one’s benefits have been directly affected so far. Regardless, it would be in the program’s best interests if the shutdown ended as soon as possible.

*********************************************************************

Listen to Anne Montgomery on our podcast episode entitled, “For Bots’ Sake, Keep AI out of Medicare!” here.

Don’t forget to watch our new historical documentary, “Social Security: 90 Years Strong.”

Related Posts