Thanks, Cato, But Let’s Not “Re-Imagine” Social Security (It’s Been Working for 90 Years)

What do you get when a libertarian think tank publishes a book proposing to radically change Social Security in collaboration mostly with other right-leaning organizations? You get something like “Re-imagining Social Security,” authored by the CATO Institute’s Ivane Nachkebia and Romina Boccia (who more than once has called the program a ‘legal Ponzi scheme’). Not surprisingly, to these authors, “re-imagining” the program that some 70 million Americans depend on for financial security essentially means altering the program beyond recognition and cutting benefits for future retirees. To which we say: better not to let their imaginations run away with our earned benefits.

The libertarian Cato Institute (which never met a federal program it liked) appears to be on a crusade to undermine the existing Social Security program. Just this week, Boccia published a post in Cato’s ‘Debt Dispatch’ blog, claiming that Social Security “operates on the Robin Hood principle in reverse.” This is, pardon the expression, quite rich coming from a think tank whose funders include the Koch network and mega-corporations like Google, Facebook, Philip Morris, the American Petroleum Institute and Chevron.

Here’s what we call “reverse Robin Hood”: a right-leaning think tank funded by financial elites striving to compromise future seniors’ earned benefits. The book and blog post are simply the latest fusillade in a decades-long campaign to discredit Social Security, arguably one of the greatest legacies of that conservative bogeyman: FDR’s New Deal. (See more about this below, including Cato’s 1983 screed, “Achieving a Leninist Strategy.”)

We do give Nachkebia and Boccia credit for raising a serious issue: the very real financial challenges facing Social Security. The program’s trustees project that the Social Security trust fund reserves will become depleted in the early 2030s – unless Congress takes pre-emptive action. The authors are simply wrong about the cause and the cure.

NCPSSM President Max Richtman (center) debates author Romina Boccia (left) about Social Security policy at a 2024 forum

The book’s first mistake is ascribing the predicted shortfall purely to ‘demographic’ changes in American society (older people becoming a bigger chunk of the population while birthrates decline), which the 1983 Social Security reforms already anticipated and addressed with a mix of revenue enhancements and benefit cuts. That is why Social Security’s full retirement age has been gradually increased from 65 to 67.

The authors ignore the current culprit – rising wealth inequality – which has been depriving Social Security of much-needed revenue for years. After all, we’re living in an age when Elon Musk, Jeff Bezos, and Mark Zuckerberg own more wealth than the bottom 50% of American society. Four decades ago, Social Security payroll taxes captured about 90% of all wages. Today, that figure has slipped to about 80%, as the wage and wealth gap widens (and higher earners make more of their money from investment income).

In 2026, annual wages exceeding $184,500 will not be subject to Social Security payroll taxes. Under this system, Musk, Bezos, and Zuckerberg will finish contributing to Social Security shortly after the ball drops in Times Square in January, while most of us pay into the program for the entire year.

The most painless and equitable fix to this problem would be to adjust – or outright eliminate – the payroll wage cap, in addition to folding-in some of wealthier earners’ non-wage income. Of course, the “Reimagining” authors do not favor this solution, because right-of-center groups do not want the wealthy to pay higher taxes for any reason. (Cato Institute and the Heritage Foundation, one of the book’s contributors, championed Trump’s 2025 massive tax giveaway for the wealthy, funded by more than $1 trillion in Medicaid and food assistance cuts. Talk about ‘Reverse Robin Hood!’)

The public appears to feel quite differently. Americans say they are willing to pay more for Social Security if it means the program will survive and thrive well into the 21st century. A survey published in 2025 by the National Academy of Social Insurance (NASI) found that a majority of Americans support eliminating the payroll wage cap on income over $400,000. Further, according to NASI, “Americans across all groups, including a majority of Republicans, say they are willing to contribute more by gradually increasing the payroll tax rate to strengthen the program’s finances.”

The right-leaning Cato Institute is funded by financial elites, including the Koch Network and Big Oil

On the other hand, the survey found that, given a “broad set of options to address Social Security’s financing gap,” Americans strongly reject benefit reductions. The public’s wishes do not seem to resonate with Cato’s authors, who advocate, among other measures:

- Raising the retirement age again

- Transitioning to a flat-benefit structure

- Indexing initial benefits to prices instead of wages

- Cutting the annual Cost-of-Living Adjustment (COLA)

Make no mistake: these proposals would cut benefits and turn Social Security into a welfare program instead of social insurance for everyone, which it was designed to be. The authors claim to have the interests of today’s younger adults in mind. Never mind that tomorrow’s seniors will rely even more on Social Security than current seniors do, thanks to the disappearance of employer-provided pensions, rising wealth inequality, and the soaring costs of everything from college tuition to medical care — making it harder for younger adults to save for retirement. (Today, only about 50% of workers have a retirement plan.)

It’s probably not a coincidence that, more than 40 years before the publication of “Reimagining Social Security,” CATO issued a white paper entitled, “Achieving A Leninist Strategy” (1983), which mapped out a scheme to undermine public support for Social Security by dividing the generations. The strategy was: convince young people that Social Security is a bad deal, making it easier to chip away at the program that many on the right have opposed since the very beginning. (1936 Republican presidential candidate Alf Landon called Social Security “a fraud on the working man.”) Some conservatives would love to see Social Security privatized so that workers’ hard-earned contributions could be funneled to Wall Street.

1936 GOP presidential candidate Alf Landon called Social Security “a fraud on the working man.”

Boccia and Nachkebia take a slightly different tack. Their core claim is that the U.S. retirement benefit system is overly generous compared to other Western nations. They analyze retirement benefits in Canada, New Zealand, Germany and Sweden and find them to be less fulsome than ours, as if to say, “These other countries don’t feel the need to support seniors on the same level as Social Security does here. Maybe we are doing too much.”

What the authors don’t mention is that these four social democracies provide more overall services and supports to their people than we do – including universal health care[1]. They also offer subsidies (for housing, transportation, heating/cooling assistance, etc.) that lower the cost of living[2]. Sweden and Germany have free college tuition, which can significantly reduce the debt burden faced by young workers. With these fundamental supports, seniors in other Western nations do not necessarily need the level of retirement benefits that Social Security provides here.

At the same time, let’s bear in mind that Social Security benefits are relatively modest. Next year’s estimated average annual retirement benefit is $24,852, only nine thousand dollars above the federal poverty line. Without Social Security, 22 million adults and dependent children would fall into poverty. Before Franklin D. Roosevelt signed Social Security into law 90 years ago, many seniors literally lived in poorhouses.

FDR wanted workers to have a “moral right” to collect Social Security (Wikimedia Commons)

The design of Social Security (which Cato is attempting to undermine) was very much intentional. It is social insurance. Everyone contributes and everyone benefits. From the beginning, FDR insisted that Social Security be earned through workers’ payroll contributions “so as to give the contributors a legal, moral, and political right to collect their (benefits).” The book’s prescriptions would upend the program’s founding principle.

While it might be in the interest of some of the book’s contributors — including the American Enterprise Institute, the Mercatus Center, and the Heritage Foundation (authors of the notorious Project 2025) — and their donors to shrink Social Security in the name of ‘saving it,’ we’re hard pressed to think of anyone else who would truly benefit. Instead of “Reimagining Social Security,” we prefer to imagine a future where the program that has worked so well for 90 years is strengthened and preserved as an earned benefit, just as FDR intended.

[1] The Commonwealth Fund, “International Health Care System Profiles”, https://www.commonwealthfund.org/international-health-policy-center/system-profiles

[2] Government of Canada, “Benefits”, https://www.canada.ca/en/services/benefits.html; KiwiEducation, “Social Benefits in New Zealand”, https://kiwieducation.com/nz/lifehack/social-benefits-in-new-zealand/; Facts About Germany, “Strong Welfare State”, https://www.tatsachen-ueber-deutschland.de/en/germany-glance/strong-welfare-state; Forsakringskassan, “Social Insurance in Sweden”, https://www.forsakringskassan.se/english/moving-to-working-studying-or-newly-arrived-in-sweden/social-insurance-in-sweden

Latest Social Security Website Crash a Symptom of Trump/DOGE Mismanagement

Seniors trying to access their earned benefit information hit a snag when the Social Security Administration’s (SSA) website crashed on Wednesday morning. These sorts of incidents have unfortunately become commonplace since the Trump administration took over, as DOGE’s crusade at SSA has left the agency in chaos.

“We continue to get reports of glitches on SSA’s website. It looks like this was one of them,” said NCPSSM President and CEO, Max Richtman.

At around 10 AM on Wednesday, My Social Security users faced “Online Service Not Available” errors. Advocates questioned whether the outage stemmed from SSA’s June login overhaul, which mandated Login.gov and ID.me as the sole sign-in options and scrapped traditional Social Security usernames and passwords. (Under new Trump administration rules, beneficiaries are no longer able to verify their identity over the phone.)

Thanks to Trump, Commissioner Frank Bisignano, and DOGE, staffing at SSA sits at historic lows, as the administration continues to force out experienced civil servants (including knowledgeable IT staff) in favor of a “technology agenda” better suited for the private sector, not an agency intended to serve the public. As a result, the website crashed five times in the month of March, and again during this latest incident. (Let’s not even get started on the AI bots that SSA has deployed to answer customer phone calls, which CNET called “maddening.”)

Trump’s Social Security Commissioner Frank Bisignano has presided over reckless cuts at SSA (AP Images)

Nancy Altman, President of Social Security Works, pointed out how Trump/DOGE cutbacks make tech outages “far more likely.” She told ThinkAdvisor, “This is especially concerning because Social Security leadership wants to reduce visitors to field offices by half, telling people to go online instead.”

“SSA is not a tech company to be gutted and sold to private equity. It is an agency that up until this year had nobly served the public, despite gross underfunding from Congress. On behalf of all Social Security beneficiaries, we lament the decline in service at SSA.” – Max Richtman, President and CEO, NCPSSM

SSA Commissioner Frank Bisignano has tried to disguise these reckless cuts as part of his “technology agenda,” using sketchy stats to cover up the fact that the administration has done nothing but kneecap the agency’s ability to function.

In an April edition of our podcast, former SSA Commissioner Martin O’Malley excoriated Trump and DOGE for taking a “meat cleaver” to what had been an improving agency under the Biden administration, despite chronic underfunding from Congress.

*************************************************************************************

Read our fact sheet on how seniors can protect themselves from chaos at SSA here

Read our fact check on Commissioner Frank Bisignano, aka “The Frankster” here

Listen to our “You Earned This” podcast here

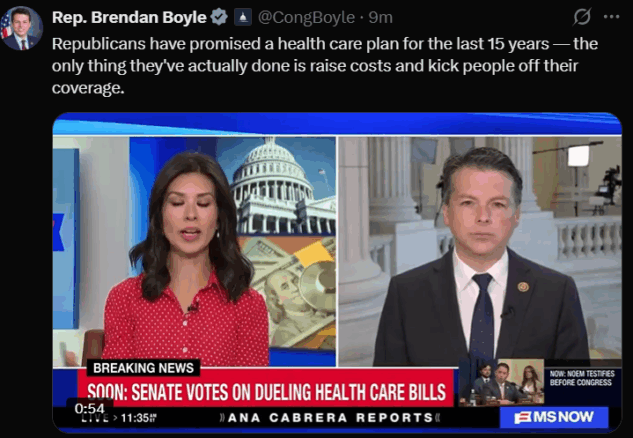

Senate Republicans Kill ACA Tax Credit Extension, Spike Health Care Premiums

Getty Images

Senate Republicans just voted to allow Americans’ health care premiums to spike in 2026, neglecting the needs of their own constituents. On Thursday, the Senate failed to reach the 60-vote threshold to extend crucial Affordable Care Act (ACA) tax credits, forcing the program’s nearly 24 million enrollees to navigate premiums that could double or even triple in 2026. In a Thursday news release, our President and CEO, Max Richtman called ACA marketplace coverage “a linchpin for older adults who often cannot get affordable health insurance any other way.”

Adults between the ages 45 and 64 account for 40 percent of ACA enrollees. Advocates worry that this group will lose their insurance and be compelled to rely on emergency room care, “a cost that gets passed on to all health care consumers,” noted Richtman. When today’s “near seniors” become eligible for Medicare at age 65, they will inevitably be in worse health than if they had been able to keep their ACA policies, putting additional strain on that program.

Following the vote, Congressman (and ‘‘You Earned This’ Podcast guest) Brendan Boyle (D-PA) excoriated Republicans for ‘kicking people off their coverage”:::

Instead of taking the commonsense step of extending the ACA tax credits, Republicans toyed with weak alternatives that would benefit big banking and insurance companies more than workers and families. The GOP alternative on offer Thursday would have replaced ACA tax credits (which have been working effectively to expand access to health insurance) with privatized Health Savings Accounts (HSA’s). According to a November 2025 report from Senate Finance Committee Democrats:::

“(The HSA) gambit would funnel funds necessary for health insurance to the nation’s largest banks and insurance companies through tax-preferred accounts, while raising premiums and decreasing payouts.” Senate Finance Committee, Minority Report

President Trump even tried to deflect this inconvenient truth during one of his signature late night tirades on Truth Social: “THE ONLY HEALTHCARE I WILL SUPPORT OR APPROVE IS SENDING THE MONEY DIRECTLY BACK TO THE PEOPLE, WITH NOTHING GOING TO THE BIG, FAT, RICH INSURANCE COMPANIES, WHO HAVE MADE $TRILLIONS, AND RIPPED OFF AMERICA LONG ENOUGH.”

Well, Mr. President, it seems as though the opposite has happened.

Rather than accept this insufficient “replacement” for expiring ACA credits, NCPSSM urges its readers to contact their representatives in Congress, and let them know you support our letter to Congress, which demands that members of the House sign a discharge petition that would bring these credits back under consideration by the chamber.

In response to consistent attacks on health coverage, progressive states have gotten creative and are trying their best to pick up the slack. In October, Maryland Governor Wes Moore unveiled the Premium Assistance Program, which will offset two-thirds of the projected ACA premium hikes.

Unfortunately, many states simply cannot make up the losses in coverage that will result from the GOP’s inaction on ACA tax credits.

“Extending these tax credits to keep Americans’ premiums from rising would have made simple common sense. Make no mistake: In 2026, older voters will remember who fought to protect their health coverage and who abdicated that responsibility.” – Max Richtman, President and CEO, NCPSSM

****************************************************************************

Find our letter to Congress supporting a discharge petition here

Find information to contact your representative in Congress here

Listen to our podcast here

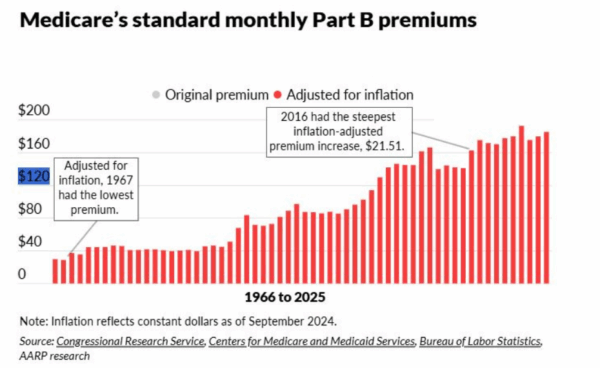

What’s Behind the Medicare Part B Premium Spike?

The nearly 67 million Americans who depend on Medicare will ring in the new year with an unwelcome cost increase. The Centers for Medicare and Medicaid Services (CMS) has announced that Part B premiums will rise to $203 per month from $185 in 2025. That $18 (or 10%) increase will consume about one-third of the average Social Security Cost-of-Living Adjustment (COLA).

“The average COLA will be $56 per month before the $18 Medicare Part B premium hike, leaving the average Social Security beneficiary with an effective monthly increase of $36 next year” noted our President and CEO Max Richtman in a news release.

Advocates and health care experts alike are worried about the impact on seniors’ ability to make ends meet. The meager COLA, less the Medicare Part B premium hike, leaves millions of seniors struggling to cover basic necessities like food, transportation, and utilities — let alone out‑of‑pocket health expenses.

“This premium jump will really pinch older Americans where it hurts,” says Anne Montgomery, our senior health policy expert. “An almost $18 premium increase may not sound huge on paper, but for people on fixed incomes, it’s a big chunk of their limited budgets.”

This one of the largest spikes in Part B premiums since 2016. While not entirely unexpected, it underscores deeper issues. As Montgomery points out, “Part B premiums are rising in part because of broader medical inflation and the cost of moving many treatments out of hospitals and into doctors’ offices and outpatient settings.”

At the same time, for–profit Medicare Advantage (MA) plans continue to exert cost pressures on the entire Medicare system. “We need to take a closer look at how Medicare Advantage is influencing overall spending,” Montgomery notes. “The way some MA plans game the system to boost profits drives up Medicare costs by billions, and those higher costs trickle down to beneficiaries in the form of higher premiums.”

A 2024 study from USC concluded that Medicare Advantage plans cost taxpayers an extra 22% per enrollee, to the tune of $83 billion a year.

We and other advocates have backed legislation to give seniors’ more relief from inflation by changing the outdated COLA formula, the CPI-W, which is based on the spending habits of urban wage earners. The current formula “undercounts the costs that weigh most heavily on older adults—especially health and prescription expenses,” says Anne Montgomery.

For years, NCPSSM has urged Congress to adopt the Consumer Price Index for the Elderly (CPI‑E) to calculate annual COLAs. The CPI‑E tracks how inflation uniquely affects Americans over 62, making it a more accurate reflection of retirees’ financial reality.

“The CPI‑E would base cost-of-living adjustments on the actual spending patterns of seniors,” says Montgomery. “An adjustment tied to the CPI‑E would more accurately protect seniors against rising healthcare costs year after year.”

“We support legislation that would adopt the CPI-E for determining COLAs, but Congress has yet to act on it. This would be a more than reasonable step toward expanding benefits to truly meet the needs of 21st century seniors.” -Max Richtman, President and CEO, NCPSSM

We urge our readers to contact their elected representatives and demand action: adopt the CPI-E formula for COLAs and curb Medicare Advantage abuses that continue to drive up health care costs for ourselves and our older loved ones.

What Does the End of the Shutdown Mean for Older Americans?

As the longest government shutdown in U.S. history finally ends, many of our readers are asking: what does this deal mean for older adults? We supported Democratic efforts to extend Affordable Care Act (ACA) premium subsidies. Without Congressional action to extend these subsidies, millions of “near seniors”— aged 54 to 65— are poised to face dramatically higher health insurance premiums in 2026.

In a statement issued when the Senate deal to end the shutdown was announced, our president and CEO, Max Richtman, warned: “Without those subsidies, ACA premiums could more than double in 2026, forcing people to endure unnecessary financial pain — or lose health coverage altogether.”

Older Americans, who already face higher premiums than younger adults, will have to navigate an even tougher road if these subsidies go by the wayside. “Their lives will be harder, and probably shorter,” says Richtman. “In addition, when those near seniors become eligible for Medicare at age 65, they will be sicker than if they had been able to keep their ACA policies, putting more of a strain on the Medicare program itself.”

As part of the deal to end the shutdown, Senate Democrats have been given a promise that the chamber will vote on a bill to extend the subsidies by the end of the second week of December. Of course, it remains to be seen whether Republicans hold up their end of the bargain. The GOP currently holds a 53-47 majority in the Senate, meaning any successful vote would require at least four GOP defections. Moderates Lisa Murkowski (R-AK), Susan Collins (R-ME), and Thom Tillis (R-NC) along with rural-state populists Josh Hawley (R-MO) and Jerry Moran (R-KS) may be potential ‘yes’ votes to extend the ACA subsidies if it comes to the floor.

Leader Jeffries & Congressional Democrats have not given up on extending ACA subsidies

There is a bit of good news in the shutdown deal for seniors on Medicare. It includes a much-needed extension of Medicare telehealth flexibilities through January 30, 2026, retroactively covering virtual visits from the shutdown period. This will provide critical relief for patients aged 65 and older, who have increasingly relied on telehealth to access care instead of burdensome, in-person doctor visits. Permanent telehealth provisions, such as those for mental health services, are also in effect — and are not impacted by this extension, notes HHS.

The deal also continues extra Medicare payments for hospitals with low patient volumes and disproportionate numbers of senior patients, and will also delay scheduled Medicare payment cuts, including for laboratory tests.

Older Americans’ lives “will be harder, and probably shorter” without ACA subsidies, says NCPSSM president Max Richtman

Unfortunately, the Medicare telehealth coverage extension is only temporary. And, of course, those crucial ACA subsidies remain in limbo for now.

“We must keep fighting to preserve those crucial ACA subsidies so that millions of the most vulnerable Americans don’t lose health coverage.” -Max Richtman, President and CEO, NCPSSM

These next few weeks present a crucial window for the health care status of ‘near seniors.’ It will be especially important for older Americans in red states and districts to make their voices heard, and let their representatives know just how important these premium subsidies are. The shutdown may be ending, but the fight for affordable health care for all Americans continues.

*******************************************************************************************************

Read about relevant policy updates from HHS here

Listen to our podcast here

Find information to contact your representative in congress here