Busting the Social Security “Greedy Geezer” Myth

One of the favorite poll-tested messages used widely by Washington’s billion dollar anti-entitlement lobby is that America’s “greedy geezers” are stealing from their grandchildren. They claim that if we allow retirees to collect the Social Security benefits they’ve contributed throughout their working lives, then somehow our children will suffer. This flawed argument assumes that every dollar these anti-Social Security crusaders would cut from Social Security benefits would then be sent to funding children’s programs, rather than reducing the deficit or cutting taxes. Which do you think is more likely?

This mythological link between funding for seniors programs and children’s programs makes for good propaganda but there’s literally no basis in reality for such linkage. We could just as easily say military spending, transportation spending or tax expenditures for the wealthy are stealing dollars from children’s programs. In fact, new research by the Center for Economic and Policy Research shows that real linkage may exist between the dollars spent on our nation’s top 1% and reduced spending on children.

Economist Dean Baker asks: Do Wall Street and the 1 Percent Thrive at the Expense of Our Kids?

“A

s a practical matter, if we look across countries we find that there is actually a positive relationship between spending on the elderly and spending on children. Countries that have been willing to commit a larger share of their output to ensuring that seniors enjoy a decent standard of living also seem willing to commit the necessary resources to ensure that their children have a good start in life.

While there may actually be no tradeoff between spending on seniors and spending on kids, there do appear to be other tradeoffs. For example, if we look at the share of GDP devoted to finance we find solid evidence of an inverse relationship with the willingness to support children.

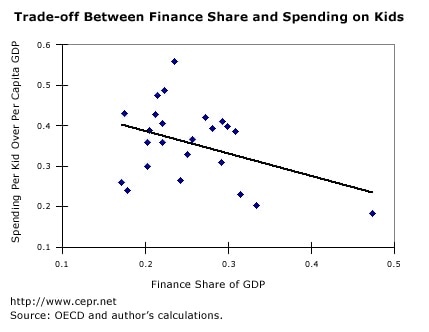

Figure 1 graphs government spending per kid divided by per capita GDP against the share of GDP originating in the financial sector. There is a significant negative relationship, meaning the larger the share of the financial sector in the economy the less money is spent on kids. (The countries are all the OECD countries for which data is available, excluding former Soviet bloc countries.)

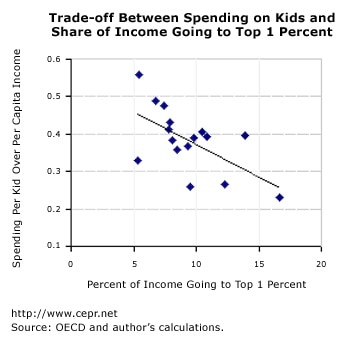

In fact, we also look at the question about the wealthy more broadly. Figure 2 shows government spending per kid divided by per capita GDP against the share of income going to the richest 1 percent. The chart includes all the countries for which data is available. In this case there is also a negative relationship with an even stronger statistical fit. The downward slope to the line is just slightly short of being significant at the 1.0 percent level.

This chart again shows a clear negative relationship, this time between the share of income going to the richest 1 percent and the amount of money that governments are willing to spend on kids. This may suggest that the richest 1 percent are not happy about supporting other people’s children through the government. In that case, the more money they are able to control, the less is likely to go to kids.”

s a practical matter, if we look across countries we find that

s a practical matter, if we look across countries we find that  The chart clearly shows that countries with larger financial sectors are less generous to their children. While this hardly proves causation (it could be that if countries spend more money on their kids they won’t go into finance), it certainly should raise questions as to whether financial interests are hostile to public spending on kids.

The chart clearly shows that countries with larger financial sectors are less generous to their children. While this hardly proves causation (it could be that if countries spend more money on their kids they won’t go into finance), it certainly should raise questions as to whether financial interests are hostile to public spending on kids.We highly recommend you read the full analysis here. Thanks to CEPR for backing up what most American families understand intuitively. Cutting benefits to generations of middle-class families won’t help the children, parents and grandparents in those families. The Recession Generation and beyond will need Social Security as much, if not more, than current generations. It’s time to reverse a 40 year trend of income inequality and redistribution to the wealthy while reigniting the American dream for middle-class families which benefits young and old alike.

Why Seniors Need a CPI-E

Max Richtman, NCPSSM President/CEO

Max Richtman, NCPSSM President/CEO

Austerity or Accuracy? Why Seniors Need a CPI-E

In 1987, while the Staff Director of the Senate Special Committee on Aging, I helped develop legislation to create a Consumer Price Index for the Elderly (CPI-E). The goal was to more accurately measure the prices and inflation seniors face, ultimately leading to more representative cost of living adjustments (COLAs) for America’s retirees. Never in my wildest dreams could I have predicted that, 26 years later, our nation would still be without an accurate CPI formula for millions of seniors, and that the CPI-E would still be considered “experimental.” Even in Washington, a quarter of a century should be enough for any experiment. It’s long past time for Congress to provide the resources needed for the Bureau of Labor Statistics (BLS) to finish it’s work on the CPI-E.

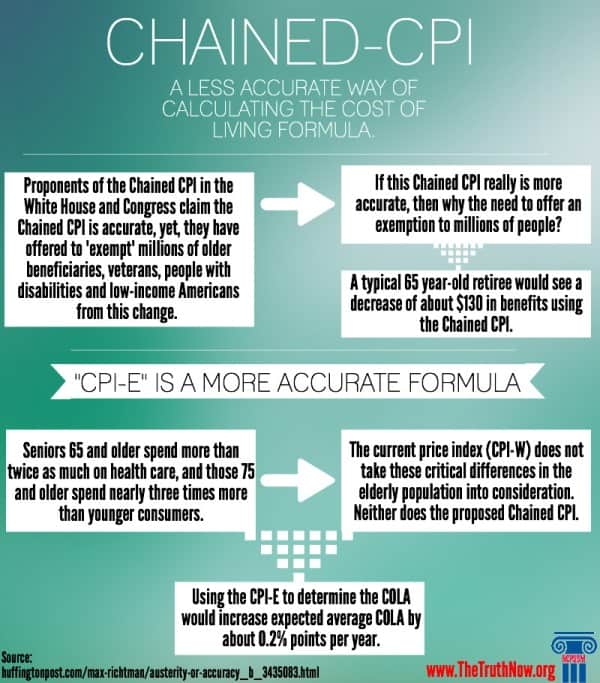

This is especially important now as many politicians in Washington hope to adopt a new formula called the chained CPI (C-CPI-U). Proponents of the C-CPI-U in the White House and Congress claim COLA accuracy is the goal, yet, they have also offered to “protect” millions of older beneficiaries, veterans, people with disabilities and low-income Americans from this change. You have to ask yourself, if this chained CPI really is more accurate, then why the need to offer an exemption to millions of people? The answer is simple. The chained CPI does not accurately measure these groups’ expenses; in fact, it makes most of the same errors as the current formula and adds a few. Adoption of this new formula is really about cutting benefits and raising taxes on average Americans to reduce the deficit.

The current formula, the CPI-W, reflects the expenditures of about 31 percent of households nationally; specifically, wage and clerical households in urban areas. By definition, this population is employed, unlike most retired Social Security beneficiaries. Research has shown that spending patterns differ between the elderly and the general population, especially on health care. Seniors 65 and older spend more than twice as much on health care, and those 75 and older spend nearly three times more than younger consumers. Not only do health care expenditures steadily increase with age but health care costs consistently rise much faster than general inflation. The current price index (CPI-W) does not take these critical differences in the elderly population into consideration. The chained CPI doubles-down on that flaw. Even worse, the proposed chained CPI will cut COLAs immediately for current and future retirees, veterans, the poor and people with disabilities.

For millions of seniors living on fixed incomes and the average $14,000 per year Social Security benefit, it’s frankly unimaginable that some in Washington believe those benefits are too generous. Our nation faces an impending retirement crisis yet rather than address that issue head-on; Washington is instead proposing cuts to the only guaranteed source of income for many retirees, Social Security. It simply makes no sense — unless your true goal is austerity not accuracy.

Contrary to claims the current COLA is too generous, the Social Security COLA has averaged just over 2% over the past five years with 0% for two of those years, far below the largest spending increase seniors face, which is spending on health care. It’s hard to imagine any one arguing with a straight face that a 0% COLA increase is too generous. But if the CPI-E determined the Social Security COLA, the expected average COLA would increase about 0.2 percentage points per year. In contrast, using the chained CPI would reduce expected average COLAs by 0.3 percentage points per year. That means a typical 65 year-old would see a decrease of about $130 in Social Security benefits using the chained CPI, three years after the C-CPI-U kicks in. At age 95, the same senior would face a 9.2 percent reduction—almost $1,400 per year. The BLS acknowledges the current CPI-W does not “produce official estimates for the rate of inflation experienced by subgroups of the population, such as the elderly or the poor. This is why we need a true elderly index like the CPI-E and not a formula change that will cut benefits and drive more seniors into poverty. A provision in Senator Bernie Sanders’s bill to reauthorize the Older Americans Act (S. 1028) would require the BLS improve the CPI-E and should be adopted by this Congress without any further delay.

According to the BLS, it needs to conduct additional research on where elderly households are located, where the elderly actually shop, and what mix of products the elderly purchase. That research will cost money but the cost to develop the CPI-E is miniscule compared to how much seniors and their families will lose without adequate inflation protection. After nearly three decades, it’s past time for Congress to provide the resources BLS needs to finish its work.

This blog post originally appeared on Huffington Post.

Cutting Social Security Targets Already Burdened Younger Workers

William Spriggs, Chief Economist at the AFL-CIO, has a terrific blog post today that we recommend to you as a must-read.

William Spriggs, Chief Economist at the AFL-CIO, has a terrific blog post today that we recommend to you as a must-read.

In Understanding the Need for Full Employment, Spriggs lays bare the absurdity of the intergenerational warfare campaign waged by the Wall Street funded anti-Social Security lobby and makes the case for the real issue we should be focusing on…unemployment, especially among young workers.

Here’s a highlight but we recommend you read the entire blog post:

“This is tangible, easy to see costs of high unemployment for young people. Unfortunately, it is money they will not make up easily. Evidence is that entering the labor market in times of high unemployment permanently lowers the earnings of workers. The downturn of the 1980s left permanent scars on the earnings of those who graduated into the labor market between 1981 and 1983. The only way for the current young workers to make up those lost earnings will be to work longer—make it up at the ends of their working lives.

But, if America would return to getting to full employment faster, young workers would benefit greatly. And, Social Security would benefit. This is the true inter-generational struggle. The current generation of politicians is ignoring the immediate and long-term needs of young workers.

Now, the perverse twist is that the debate is on cutting the Social Security benefits of future retirees—meaning the current set of young workers who are suffering the most from high unemployment. The same set of young people who are not building up the savings needed to help them when they are old.

Here, the Social Security Trust Fund report is helpful. The report says that Social Security is currently taking in more money than it is paying out—revenue from current taxes and interest on the Trust Fund are more than current outlays to pay benefits. So, the Trust fund is continuing to grow. The Trust Fund is large enough to pay all promised benefits until 2033. That means well past when the first wave of the Baby Boomers—those born before 1949—will be finished receiving benefits—more crudely, when they are dead. This means the current jargon on intergenerational transfer is a false debate; making it appear the AARP is trying to squeeze money out of young workers.

Instead, those who are fighting to protect Social Security—like the National Committee to Preserve Social Security and Medicare—are really fighting for today’s young workers. Protecting Social Security is making sure that young workers do not have to pay for the nearsightedness of austerity budgets that cheat the young out of policy debates on generating jobs, and then make young workers pay in retirement because of that same world view.”

So, the next time you hear our nation’s wealthiest CEO’s and Wall Street millionaires as part of their billion dollar lobby campaign led by “Fix the Debt”, the Business Roundtable (and countless other Pete Peterson backed organizations) decrying, “What kind of nation are we leaving our children?” while suggesting that shredding their retirement safety net somehow makes it better, we hope people will ask one simple question: “What’s your plan to create jobs for our young workers?”

The silence could be deafening.

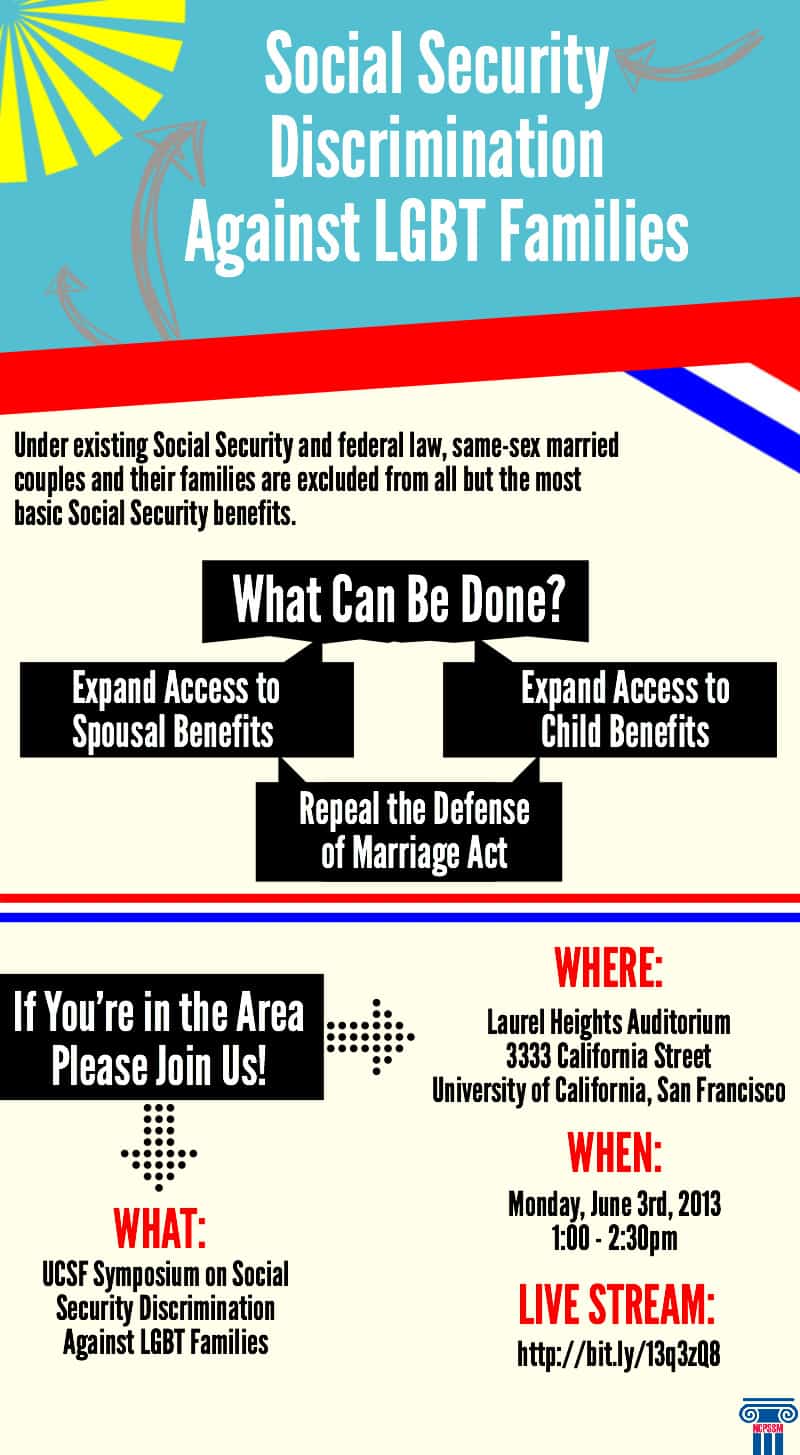

Living Outside the Safety Net

You may not realize it but same-sex couples and their families across the country are denied a host of benefits that are routinely provided to heterosexual couples. even as more and more states now provide legal recognition for same-sex couples. The Defense of Marriage Act (DOMA) prevents these relationships from being recognized for Social Security family and spousal benefits. as a result, same-sex couples and their families continue to be excluded from all but the most basic Social Security benefits.

We believe that the time has come to extend the benefits the social security program provides to reflect the changing face and needs of the American workforce. That is why both the HRC and NCPSSM Foundations urge Congress to revise the Social Security Act and to repeal DOMA to ensure that LGBT workers and their families have equal access to these vital benefits. This is a matter of simple fairness. Lesbian, gay, bisexual, and transgender people are vital members of the American workforce and contribute their equal share to the social security system with every paycheck. Now is the time to ensure equal access to benefits.

The National Committee is proud to co-host a symposium in California today to talk about these issues and our report, co-authored with the Human Rights Campaign, entitled “Living Outside the Safety Net: LGBT families and Social Security.”

Even if you don’t live in California you can still watch the event live today from here.

Sorting Fact from Fiction in the 2013 Trustees Report on Social Security and Medicare

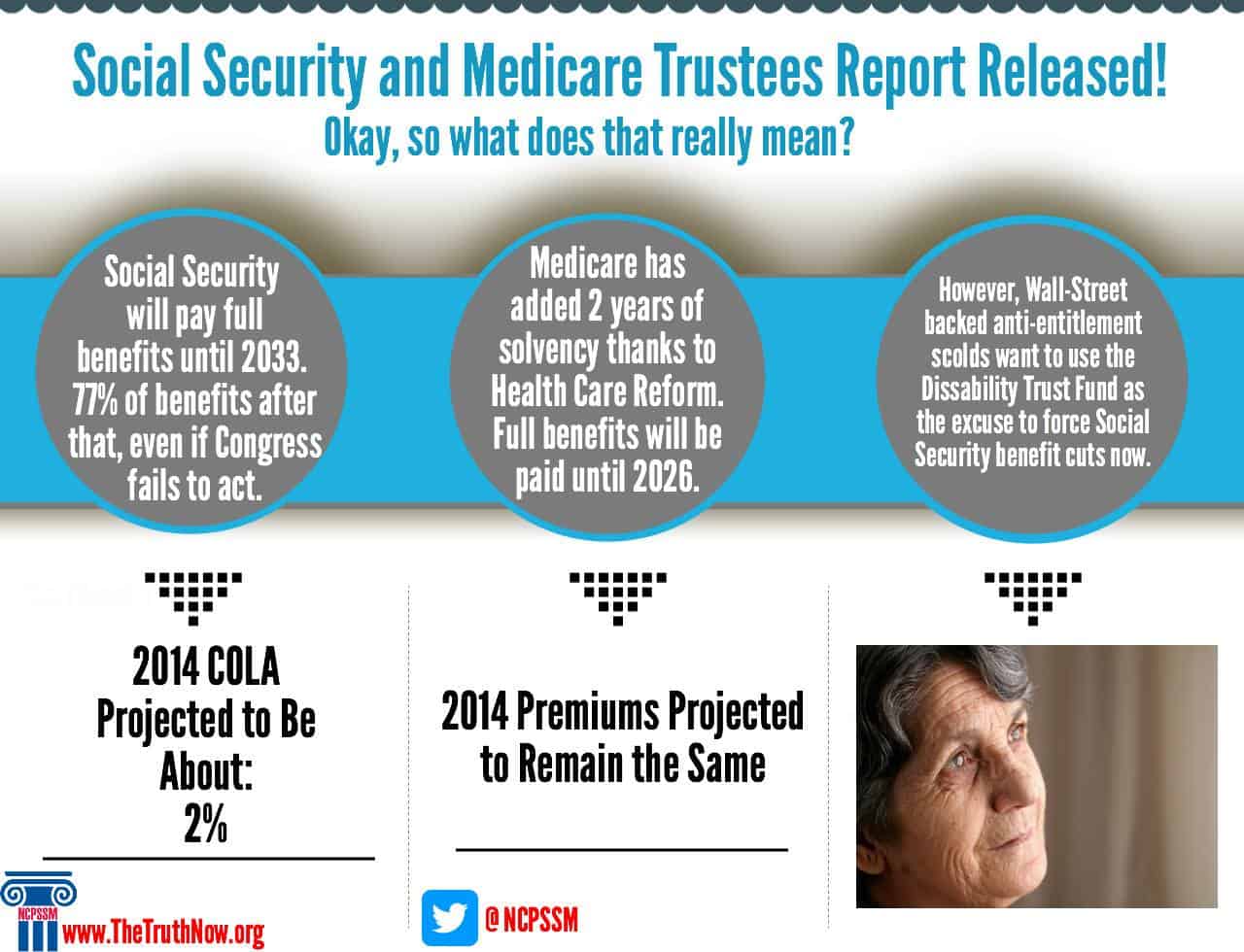

The 2013 Trustees report shows, once again, Social Security is not facing a crisis.

The 2013 Trustees report shows, once again, Social Security is not facing a crisis.

- Trustees project Social Security will be able to pay full benefits until the year 2033. After that, Social Security will have sufficient revenue to pay 77% of benefits.

- Social Security is still well funded. In 2013, as the economy regains its footing, Social Security’s total income is projected to exceed its expenses. In fact, the Trustees estimate that total annual income will exceed program obligations until 2020.

- Trustees project a Cost of Living Adjustment increase of 1.5% to 2.5% in 2014.

With so little bad news to report in this 2013 Trustees report, critics have now shifted their attention to Social Security Disability, which faces a more immediate fiscal challenge

- Trustees project the Disability Trust fund will be depleted in 2016, the same year projected in last year’s report. This projected shortfall is not a surprise and Congress should reallocate income across the Social Security Trust funds, as it has done 11 times before, to cover the anticipated shortfall. Disability expenditures have increased primarily due to demographic trends. The increase in full retirement age from 65 to 66 has also contributed to the increase in disability expenditures, as people remain on the disability rolls longer before shifting to retirement. However, when Congress took action in 1994 to address a then-reported shortfall in DI, it knew that it would have to take action again in 2015 or 2016.

The 2013 Trustees report shows slowing the growth of health care costs has improved Medicare’s Trust Fund.

- Medicare solvency remains greatly improved thanks to passage of healthcare reform, with the program paying full benefits until 2026, two years later than the 2012 report. Health care spending has also grown much more slowly. Since late 2010, CBO has reduced its projection of cumulative Medicare and Medicaid spending over the 2011-2020 period by $900 billion – or nearly 10 percent.

- Medicare Part B premiums are not projected to increase in 2014.

Here’s reaction from NCPSSM’s President/CEO, Max Richtman:

“As we emerge from the worst economic downturn since the Great Depression, it’s clear our nation’s retirement security programs, Social Security and Medicare, continue to do their jobs admirably by protecting millions of Americans during these troubled times. Unfortunately, for too many in Washington, this annual Trustees report is little more than an opportunity to re-issue the same doom-and-gloom news releases and renewed calls to cut these programs in order to ‘save’ them, regardless of the fiscal facts. The truth is the Trustees 2013 report shows Social Security has a $2.7 trillion surplus which continues to grow. Social Security isn’t bankrupt; it hasn’t contributed a dime to our fiscal woes and, in fact, has performed its mission without fail.

On the Medicare front, the good news is health care reform has extended the solvency of the Medicare Trust Fund and health care cost growth is slowing. The Affordable Care Act is making a difference not just in Medicare, but is also slowing the rising cost of health care for all Americans.”

Busting the Social Security “Greedy Geezer” Myth

One of the favorite poll-tested messages used widely by Washington’s billion dollar anti-entitlement lobby is that America’s “greedy geezers” are stealing from their grandchildren. They claim that if we allow retirees to collect the Social Security benefits they’ve contributed throughout their working lives, then somehow our children will suffer. This flawed argument assumes that every dollar these anti-Social Security crusaders would cut from Social Security benefits would then be sent to funding children’s programs, rather than reducing the deficit or cutting taxes. Which do you think is more likely?

This mythological link between funding for seniors programs and children’s programs makes for good propaganda but there’s literally no basis in reality for such linkage. We could just as easily say military spending, transportation spending or tax expenditures for the wealthy are stealing dollars from children’s programs. In fact, new research by the Center for Economic and Policy Research shows that real linkage may exist between the dollars spent on our nation’s top 1% and reduced spending on children.

Economist Dean Baker asks: Do Wall Street and the 1 Percent Thrive at the Expense of Our Kids?

“A

While there may actually be no tradeoff between spending on seniors and spending on kids, there do appear to be other tradeoffs. For example, if we look at the share of GDP devoted to finance we find solid evidence of an inverse relationship with the willingness to support children.

Figure 1 graphs government spending per kid divided by per capita GDP against the share of GDP originating in the financial sector. There is a significant negative relationship, meaning the larger the share of the financial sector in the economy the less money is spent on kids. (The countries are all the OECD countries for which data is available, excluding former Soviet bloc countries.)

In fact, we also look at the question about the wealthy more broadly. Figure 2 shows government spending per kid divided by per capita GDP against the share of income going to the richest 1 percent. The chart includes all the countries for which data is available. In this case there is also a negative relationship with an even stronger statistical fit. The downward slope to the line is just slightly short of being significant at the 1.0 percent level.

This chart again shows a clear negative relationship, this time between the share of income going to the richest 1 percent and the amount of money that governments are willing to spend on kids. This may suggest that the richest 1 percent are not happy about supporting other people’s children through the government. In that case, the more money they are able to control, the less is likely to go to kids.”

We highly recommend you read the full analysis here. Thanks to CEPR for backing up what most American families understand intuitively. Cutting benefits to generations of middle-class families won’t help the children, parents and grandparents in those families. The Recession Generation and beyond will need Social Security as much, if not more, than current generations. It’s time to reverse a 40 year trend of income inequality and redistribution to the wealthy while reigniting the American dream for middle-class families which benefits young and old alike.

Why Seniors Need a CPI-E

Max Richtman, NCPSSM President/CEO

Austerity or Accuracy? Why Seniors Need a CPI-E

In 1987, while the Staff Director of the Senate Special Committee on Aging, I helped develop legislation to create a Consumer Price Index for the Elderly (CPI-E). The goal was to more accurately measure the prices and inflation seniors face, ultimately leading to more representative cost of living adjustments (COLAs) for America’s retirees. Never in my wildest dreams could I have predicted that, 26 years later, our nation would still be without an accurate CPI formula for millions of seniors, and that the CPI-E would still be considered “experimental.” Even in Washington, a quarter of a century should be enough for any experiment. It’s long past time for Congress to provide the resources needed for the Bureau of Labor Statistics (BLS) to finish it’s work on the CPI-E.

This is especially important now as many politicians in Washington hope to adopt a new formula called the chained CPI (C-CPI-U). Proponents of the C-CPI-U in the White House and Congress claim COLA accuracy is the goal, yet, they have also offered to “protect” millions of older beneficiaries, veterans, people with disabilities and low-income Americans from this change. You have to ask yourself, if this chained CPI really is more accurate, then why the need to offer an exemption to millions of people? The answer is simple. The chained CPI does not accurately measure these groups’ expenses; in fact, it makes most of the same errors as the current formula and adds a few. Adoption of this new formula is really about cutting benefits and raising taxes on average Americans to reduce the deficit.

The current formula, the CPI-W, reflects the expenditures of about 31 percent of households nationally; specifically, wage and clerical households in urban areas. By definition, this population is employed, unlike most retired Social Security beneficiaries. Research has shown that spending patterns differ between the elderly and the general population, especially on health care. Seniors 65 and older spend more than twice as much on health care, and those 75 and older spend nearly three times more than younger consumers. Not only do health care expenditures steadily increase with age but health care costs consistently rise much faster than general inflation. The current price index (CPI-W) does not take these critical differences in the elderly population into consideration. The chained CPI doubles-down on that flaw. Even worse, the proposed chained CPI will cut COLAs immediately for current and future retirees, veterans, the poor and people with disabilities.

For millions of seniors living on fixed incomes and the average $14,000 per year Social Security benefit, it’s frankly unimaginable that some in Washington believe those benefits are too generous. Our nation faces an impending retirement crisis yet rather than address that issue head-on; Washington is instead proposing cuts to the only guaranteed source of income for many retirees, Social Security. It simply makes no sense — unless your true goal is austerity not accuracy.

Contrary to claims the current COLA is too generous, the Social Security COLA has averaged just over 2% over the past five years with 0% for two of those years, far below the largest spending increase seniors face, which is spending on health care. It’s hard to imagine any one arguing with a straight face that a 0% COLA increase is too generous. But if the CPI-E determined the Social Security COLA, the expected average COLA would increase about 0.2 percentage points per year. In contrast, using the chained CPI would reduce expected average COLAs by 0.3 percentage points per year. That means a typical 65 year-old would see a decrease of about $130 in Social Security benefits using the chained CPI, three years after the C-CPI-U kicks in. At age 95, the same senior would face a 9.2 percent reduction—almost $1,400 per year. The BLS acknowledges the current CPI-W does not “produce official estimates for the rate of inflation experienced by subgroups of the population, such as the elderly or the poor. This is why we need a true elderly index like the CPI-E and not a formula change that will cut benefits and drive more seniors into poverty. A provision in Senator Bernie Sanders’s bill to reauthorize the Older Americans Act (S. 1028) would require the BLS improve the CPI-E and should be adopted by this Congress without any further delay.

According to the BLS, it needs to conduct additional research on where elderly households are located, where the elderly actually shop, and what mix of products the elderly purchase. That research will cost money but the cost to develop the CPI-E is miniscule compared to how much seniors and their families will lose without adequate inflation protection. After nearly three decades, it’s past time for Congress to provide the resources BLS needs to finish its work.

This blog post originally appeared on Huffington Post.

Cutting Social Security Targets Already Burdened Younger Workers

William Spriggs, Chief Economist at the AFL-CIO, has a terrific blog post today that we recommend to you as a must-read.

In Understanding the Need for Full Employment, Spriggs lays bare the absurdity of the intergenerational warfare campaign waged by the Wall Street funded anti-Social Security lobby and makes the case for the real issue we should be focusing on…unemployment, especially among young workers.

Here’s a highlight but we recommend you read the entire blog post:

“This is tangible, easy to see costs of high unemployment for young people. Unfortunately, it is money they will not make up easily. Evidence is that entering the labor market in times of high unemployment permanently lowers the earnings of workers. The downturn of the 1980s left permanent scars on the earnings of those who graduated into the labor market between 1981 and 1983. The only way for the current young workers to make up those lost earnings will be to work longer—make it up at the ends of their working lives.

But, if America would return to getting to full employment faster, young workers would benefit greatly. And, Social Security would benefit. This is the true inter-generational struggle. The current generation of politicians is ignoring the immediate and long-term needs of young workers.

Now, the perverse twist is that the debate is on cutting the Social Security benefits of future retirees—meaning the current set of young workers who are suffering the most from high unemployment. The same set of young people who are not building up the savings needed to help them when they are old.

Here, the Social Security Trust Fund report is helpful. The report says that Social Security is currently taking in more money than it is paying out—revenue from current taxes and interest on the Trust Fund are more than current outlays to pay benefits. So, the Trust fund is continuing to grow. The Trust Fund is large enough to pay all promised benefits until 2033. That means well past when the first wave of the Baby Boomers—those born before 1949—will be finished receiving benefits—more crudely, when they are dead. This means the current jargon on intergenerational transfer is a false debate; making it appear the AARP is trying to squeeze money out of young workers.

Instead, those who are fighting to protect Social Security—like the National Committee to Preserve Social Security and Medicare—are really fighting for today’s young workers. Protecting Social Security is making sure that young workers do not have to pay for the nearsightedness of austerity budgets that cheat the young out of policy debates on generating jobs, and then make young workers pay in retirement because of that same world view.”

So, the next time you hear our nation’s wealthiest CEO’s and Wall Street millionaires as part of their billion dollar lobby campaign led by “Fix the Debt”, the Business Roundtable (and countless other Pete Peterson backed organizations) decrying, “What kind of nation are we leaving our children?” while suggesting that shredding their retirement safety net somehow makes it better, we hope people will ask one simple question: “What’s your plan to create jobs for our young workers?”

The silence could be deafening.

Living Outside the Safety Net

You may not realize it but same-sex couples and their families across the country are denied a host of benefits that are routinely provided to heterosexual couples. even as more and more states now provide legal recognition for same-sex couples. The Defense of Marriage Act (DOMA) prevents these relationships from being recognized for Social Security family and spousal benefits. as a result, same-sex couples and their families continue to be excluded from all but the most basic Social Security benefits.

We believe that the time has come to extend the benefits the social security program provides to reflect the changing face and needs of the American workforce. That is why both the HRC and NCPSSM Foundations urge Congress to revise the Social Security Act and to repeal DOMA to ensure that LGBT workers and their families have equal access to these vital benefits. This is a matter of simple fairness. Lesbian, gay, bisexual, and transgender people are vital members of the American workforce and contribute their equal share to the social security system with every paycheck. Now is the time to ensure equal access to benefits.

The National Committee is proud to co-host a symposium in California today to talk about these issues and our report, co-authored with the Human Rights Campaign, entitled “Living Outside the Safety Net: LGBT families and Social Security.”

Even if you don’t live in California you can still watch the event live today from here.

Sorting Fact from Fiction in the 2013 Trustees Report on Social Security and Medicare

The 2013 Trustees report shows, once again, Social Security is not facing a crisis.

- Trustees project Social Security will be able to pay full benefits until the year 2033. After that, Social Security will have sufficient revenue to pay 77% of benefits.

- Social Security is still well funded. In 2013, as the economy regains its footing, Social Security’s total income is projected to exceed its expenses. In fact, the Trustees estimate that total annual income will exceed program obligations until 2020.

- Trustees project a Cost of Living Adjustment increase of 1.5% to 2.5% in 2014.

With so little bad news to report in this 2013 Trustees report, critics have now shifted their attention to Social Security Disability, which faces a more immediate fiscal challenge

- Trustees project the Disability Trust fund will be depleted in 2016, the same year projected in last year’s report. This projected shortfall is not a surprise and Congress should reallocate income across the Social Security Trust funds, as it has done 11 times before, to cover the anticipated shortfall. Disability expenditures have increased primarily due to demographic trends. The increase in full retirement age from 65 to 66 has also contributed to the increase in disability expenditures, as people remain on the disability rolls longer before shifting to retirement. However, when Congress took action in 1994 to address a then-reported shortfall in DI, it knew that it would have to take action again in 2015 or 2016.

The 2013 Trustees report shows slowing the growth of health care costs has improved Medicare’s Trust Fund.

- Medicare solvency remains greatly improved thanks to passage of healthcare reform, with the program paying full benefits until 2026, two years later than the 2012 report. Health care spending has also grown much more slowly. Since late 2010, CBO has reduced its projection of cumulative Medicare and Medicaid spending over the 2011-2020 period by $900 billion – or nearly 10 percent.

- Medicare Part B premiums are not projected to increase in 2014.

Here’s reaction from NCPSSM’s President/CEO, Max Richtman:

“As we emerge from the worst economic downturn since the Great Depression, it’s clear our nation’s retirement security programs, Social Security and Medicare, continue to do their jobs admirably by protecting millions of Americans during these troubled times. Unfortunately, for too many in Washington, this annual Trustees report is little more than an opportunity to re-issue the same doom-and-gloom news releases and renewed calls to cut these programs in order to ‘save’ them, regardless of the fiscal facts. The truth is the Trustees 2013 report shows Social Security has a $2.7 trillion surplus which continues to grow. Social Security isn’t bankrupt; it hasn’t contributed a dime to our fiscal woes and, in fact, has performed its mission without fail.

On the Medicare front, the good news is health care reform has extended the solvency of the Medicare Trust Fund and health care cost growth is slowing. The Affordable Care Act is making a difference not just in Medicare, but is also slowing the rising cost of health care for all Americans.”