- Published On: July 14th, 2026Categories: ageism, Equal Time, Medicare, Social Security

In his latest column for The Atlantic titled “An Oligarchy of Old People,” author Idrees Kahloon correctly identifies a troubling symptom of the 21st century economy — a younger generation left worse off than those who came before them — while misdiagnosing the cause.

Rather than identifying the true culprit, namely wealth inequality and the concentration of power at the very top of the economic food chain, the article shifts blame to older Americans as some sort of monolithic class, regardless of income. This kind of scapegoating is exactly what (middle-aged!) finance and tech oligarchs like Thiel, Musk, Zuckerberg, and other billionaires want.

In fact, that same group has repeatedly sought to sow division and redirect blame for income inequality toward immigrants, minorities, and now older Americans. Kahloon plays into that narrative by framing the problem as “Boomers vs. everyone else,” rather than “the wealthy elite vs. everyone else,” needlessly pitting generations against each other.

Many in the media are trying to pit the generations against each other

The simple facts are that older people of varying income levels generally have a higher net worth and more assets than their younger counterparts. This is a normal feature of a functioning economy.

Ultimately, what we have seen over the last 50 years is a consistent decline in wealth equality and workers’ rights across the board. The built-in disparity between young and old has not been created by Social Security and Medicare; rather, it has grown because of broader structural forces (which we will get into later).

Now, let’s take a look at some of Kahloon’s claims, particularly those that touch on Social Security and Medicare.

“In 1965, Medicare was created. A major expansion of Social Security followed in 1972. These changes were remarkably effective: The share of elderly people living in poverty dropped by more than one-third within a decade. But because these programs are broad-based entitlements, they have transferred huge sums to the prosperous, too. The portfolios of that latter group, meanwhile, have been swelled by a rising stock market and rising home values, outcomes that may not be entirely replicable for younger generations. As a result of all of these factors, intergenerational inequality between old and young has not merely reversed. It has accelerated.”

Mr. Kahloon is correct that the changes made by FDR’s “New Deal” and LBJ’s “Great Society” were “remarkably effective” and remain so. In fact, Social Security and Medicare are the most successful anti-poverty programs in American history. But the article makes a huge leap in citing Social Security and Medicare as the main factors behind the rise in intergenerational inequality. The grounds for that causal claim are shaky at best.

LBJ signs Medicare and Medicaid into law in 1965

The real drivers of rising wealth concentration and intergenerational disparity (aka the oligarchs) are far more to blame than Americans’ earned benefits. The last several decades have seen:

- Decline of unions and labor’s bargaining power: Union coverage has fallen dramatically since the 1970s, weakening wage growth, reducing retirement benefits, and shifting power from workers to owners.

- Rising top incomes of “superstars,” finance, and executive pay: The share of income going to the top 1% and 0.1% has exploded, driven by finance, tech, and corporate governance changes that reward executives and shareholders far more than workers.

- Tax and transfer policy changes: Since the 1970s, effective tax rates on the very top earners fell substantially. For the top 0.01%, the effective federal tax rate dropped from about 59% in 1979 to 35% in 2004. Today, that number sits at a staggeringly low 24%. Meanwhile, middle-class and working-class families faced rising costs in every area of importance: Housing, education, and health care, with fewer public supports.

Social Security and Medicare have reduced old-age poverty and provided baseline income for seniors on fixed incomes. They are not the cause of rising wealth inequality, and without them, 40% of seniors would slip into poverty, while even more would lose their health care.

Taking a more cultural view, Kahloon opines that:

“Respect for elders is being replaced by resentment of elders. A majority of young Americans no longer believe in the American dream. Many Millennials and Gen Zers expressly blame the Boomers for that, accusing them of hoarding wealth, jobs, and power. Many of these accusations are inchoate, but they are not entirely baseless.”

These accusations are in fact, inchoate — and baseless, but Kahloon does nothing to correct that. Instead, it appears the author would rather further stoke these fears and divisions than place blame on the real culprits. Doing so might upset The Atlantic’s primary owners/investors — the Emerson Collective — a venture capital firm also known for its involvement in the AI, Crypto, and oil industries.

Blaming “Boomers” as a class allows the real architects of inequality (like the Emerson Collective) to avoid scrutiny. It lets them redirect anger from the concentration of wealth and power at the top to a generational fight between older and younger workers. No wonder ageism in this country remains rampant.

Finally, Kahloon suggests:

“An intergenerational recalibration can come about in gentler ways than Moyn’s: The wealthiest Social Security recipients, for instance, could forgo some of their scheduled benefits, which could instead be contributed annually to “baby bond” accounts for America’s children.”

This is a classic straw man that is nothing more than a call for means-testing Social Security benefits. As we’ve argued before, means-testing undermines the very nature of Social Security, which is social insurance, not welfare. It is designed to be universal, tied to work and contributions, and protected from the political whims that target traditional welfare programs.

It’s in the interest of America’s oligarchs to divide the generations

Once that dam breaks, Social Security will become like any other welfare program, subject to cuts whenever Republicans control Congress and the White House. To save significant money, means testing would have to cut deep into the heart of the middle class.

Slashing Social Security and Medicare to address wealth inequality would do nothing to address the core issues and causes of inequality. In fact, many conservatives want to slash the social safety net (See the massive cuts to Medicaid and food assistance in Trump’s Big, Ugly Bill), while stoking divisions among us. The real fight is not old vs. young. It is workers and families vs. financial elites that benefit from a K-shaped economy – and a distracted populace arguing over generational differences.

****************************

Listen to our podcast interview about ageism in America with expert S. Jay Olshansky here. - Published On: July 7th, 2026Categories: GOP, President Trump, privatization, Social Security

After turning the page on his self-indulgent USA250 bonanza, marred by extreme heat and disappointing attendance, President Trump has once again set his sights on Americans’ earned retirement benefits. On Monday, he announced that his administration is “working on a plan” to create accounts for adults loosely inspired by Australia’s retirement savings system – and similar to the Trump accounts for children.

Our president and CEO Max Richtman told MarketWatch today that Trump should be working on strengthening Social Security instead of “toying around” with federally-seeded private accounts.

“We would advise President Trump to focus on Social Security – a program that has worked splendidly for more than 90 years to provide Americans with basic retirement security” – Max Richtman, President and CEO, NCPSSM

Far from fortifying Social Security for the future, these private Trump accounts are a ‘back door way’ of privatizing Social Security. First, Treasury Secretary Bessent admitted as much; then, Senator Ted Cruz affirmed the “dirty little secret” of how these accounts will lead to privatization.

The push for Trump accounts is not coming from seniors’ advocates – or even from seniors themselves. Rather, it seems to be the brainchild of Bessent and Commerce Secretary Howard Lutnick. Fox Business News reports that these two cabinet members are fleshing out the private retirement plan proposal.

Uncoincidentally, Bessent and Lutnick are entangled with Wall Street. For them, a new “retirement account” system is a chance to expand the pool of money flowing into private investment products — and shift more retirement risk from the government to individuals.

This might make billionaires and Republican donors in the financial sector happy, but for the retirees who rely on Social Security for all or most of their income, the risk is simply too great to bear. In a privatized system, one bad year in the markets could lead to a 30% benefit decrease.

The Trump children’s accounts snuck through in the Big, Ugly Bill, whose main purpose was to slash social services while showering the wealthy with new tax breaks. Under the pilot program from the 2025 megabill, the federal government seeds each children’s account with $1,000. That money is then invested in a Wall Street fund, to which parents can also contribute. It’s a handy way to funnel taxpayer dollars to the financial markets, when private-sector savings plans for children (and adults, for that matter) already exist. Much like Trump Rx, the president has co-opted an extant private sector function and branded it as his own.

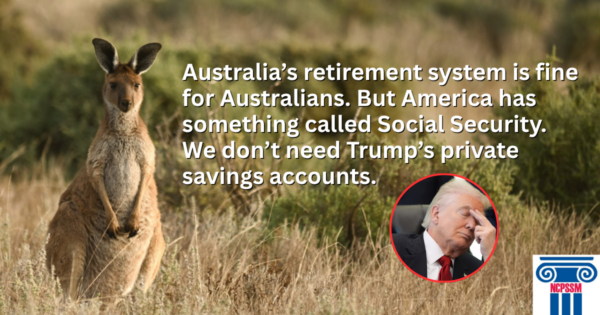

Now, Trump is recycling that branding for adults by piggy-backing off of Australia’s model – apparently without understanding the Australian model in the least. The key difference is that Australia’s plan is backed by mandated employer contributions rather than federal seed money. Australia’s retirement system, called superannuation, is built on a few simple principles:

*Employers must contribute 12% of an employee’s pay into a retirement account that the worker owns.

*Contributions go into a personal, market-invested account tied to the worker, not into a government pool.

*The system is designed to supplement Australia’s public pension, not replace it.

American employers (including many GOP donors) probably would not be thrilled to pay 12% of workers’ earnings into a new, Australian-style retirement system. U.S. employers already contribute 6.2% of wages to Social Security, matching their employees’ contributions. As Max Richtman points out, “Australia’s retirement system may be fine for Australians, but we already have a proven federal retirement program that deserves the President’s attention.” So here’s an idea: why don’t we stick with Social Security, which, with some common-sense improvements, can remain the sturdy financial lifeline that it has been for more than 90 years – instead of banking on yet another Trump branding scheme?

***************************************’

Watch our health policy expert Anne Montgomery’s takedown of Trump Rx HERE.

Read an article featuring our President & CEO’s thoughts HERE

Listen to our “You Earned This!” Podcast HERE

- Published On: July 1st, 2026Categories: Boost Social Security, Senator Elizabeth Warren, Social Security, Social Security on the Ballot, Social Security Trust Fund

Senators Bernie Moreno (R-OH) and Elizabeth Warren (D-MA)

Social Security is back in the headlines this summer, driven by both hopeful developments and urgent warnings. In the wake of the Trustees report in June, Senators Elizabeth Warren (D-MA) and Bernie Moreno (R-OH), announced a bipartisan proposal to adjust the Social Security payroll wage cap and stabilize the program’s revenue ahead of looming insolvency in the early 2030s.

Moreno’s participation in a plan to increase Social Security revenue is particularly notable – and is the first of its kind from a Republican on Capitol Hill in recent memory. This is an encouraging signal that protecting Social Security benefits can bring people together across party lines. (Bipartisan majorities of Americans favor increasing revenue flowing into the system instead of reducing benefits, even if it means paying more in Social Security payroll taxes.) It also underscores something advocates have been saying for years: the best way to preserve Social Security is not by cutting it, but by demanding that the wealthiest Americans contribute their fair share.

“We have long supported adjusting the payroll wage cap so that the wealthy contribute their fair share to Social Security. ‘Scrapping the cap’ is a far more equitable way to restore the program to long-term solvency than cutting benefits (by raising the retirement age, means testing, shrinking cost-of-living adjustments, or any other way).” – Max Richtman, President and CEO, NCPSSM

The timing of this bipartisan push is no accident. Social Security has been back in the spotlight since the Social Security Trustees released their annual report earlier last month, which projects that the depletion date of the program’s trust fund could come as early as 2032, unless Congress takes action.

That’s why it’s notable that a few conservatives have begun to acknowledge the basic fairness of scrapping the cap. Marc Goldwein, senior vice president of the (right-leaning) Committee for a Responsible Federal Budget (CRFB) called the Senators’ proposal a “perfectly reasonable” idea. Among congressional Republicans, however, Senator Moreno remains an outlier. Look no further than Speaker Mike Johnson, who declared in a recent radio show appearance that “entitlement programs… like Social Security” are “the problem” and need to be “adjusted.” He said that Republicans have a plan to “fix” Social Security next year. We can only imagine that these unspecified ‘fixes’ include GOP favorites like raising the retirement age, means testing benefits, or lowering the COLA formula — all of which are benefit cuts.

That is exactly why we launched a new voter education campaign titled, Social Security on the Ballot. “Social Security is literally on the political calendar now, because the senators elected this cycle likely still will be in office when the trust fund deadline arrives,” said Political Director Luke Warren in our most recent episode of Capital Quick Takes. He also made the point that this campaign is about raising ‘salience’ — moving Social Security from the background into the center of public dialogue, where it belongs. “Voters should know which candidates are prepared to protect earned benefits and which ones are open to cutting them” added Warren.

The point is simple: this election will determine whether Congress protects beneficiaries or cuts benefits. Seniors, families, workers, and future Social Security recipients all deserve to know where candidates stand before they vote. As our President and CEO says, “Claiming you support Social Security is not enough. Every politician says that. The question is: will you vote to expand and strengthen the program, or cut and privatize it?”

***************************************

Read Senator Warren and Moreno’s New York Times Op-Ed HERE

Watch the latest episode of Capital Quick Takes with political director Luke Warren HERE

Read our analysis of the 2026 Social Security Trustees report HERE

- Published On: June 16th, 2026Categories: Congress, Democrats, Election 2026, GOP, Social Security, Trump, Trump Administration

Istock photo

Every election year seems to be “the most important one in our lifetimes” – or the “most consequential election ever.” But… this election year really IS extremely pivotal for Social Security. That’s because the next Congress will no doubt begin grappling with the challenge of strengthening Social Security’s finances before the projected depletion of the trust fund in the early 2030’s.

In fact, U.S. Senators elected this year likely still will be in office through the end of 2032, when the trust fund will be on the precipice of insolvency… absent congressional action. Unless Congress wants beneficiaries to suffer an automatic 17-22% cut in benefits – it will have to act soon. Few who remember the reforms of 1983 want to see lawmakers once again wait until the very last minute, when options are more limited and costs steeper.

With that in mind, we have launched a new voter education campaign called “Social Security on the Ballot.” Its message is simple but urgent: when Americans go to the polls this November, they’ll be choosing candidates who will shape the future of Social Security.

As our President and CEO Max Richtman puts it:

“The stakes for current and future seniors couldn’t be higher. Depending on the composition of the next Congress, Social Security could be strengthened (and expanded) – or radically cut and privatized. It all depends on which course Congress takes, and that depends on your vote.” – Max Richtman, President & CEO, NCPSSM

Many, but not all, Republicans have staked out the position that Social Security should be cut in some way in order to restore solvency. They do not call their proposals “benefit cuts,” because that would be wildly unpopular. Instead, they speak of raising the retirement age, means testing, and lowering Social Security cost-of-living adjustments (or COLAs) – which are all benefit cuts!

Just last week, House Speaker Mike Johnson said that “entitlements” like Social Security are “a problem” – promising that Republicans have a “plan” to “fix it” next year. Though he didn’t specify what the GOP “plan” is, his remarks sent shivers up the spines of Social Security supporters. And rightly so.

Prominent Republicans also have raised the specter of privatizing Social Security – aka gambling workers’ payroll contributions on Wall Street. Last year, U.S. Treasury Secretary Scott Bessent admitted that Trump savings accounts for children actually were a “backdoor way of privatizing Social Security.”

In May, Senator Ted Cruz concurred that the Trump accounts were a Trojan Horse for privatization, calling it a “dirty little secret.” Not so secret anymore.

Senator Ted Cruz (left) & Treasury Secretary Scott Bessent (right) admit that the Trump administration is hoping to privatize Social Security (Wikimedia Commons/Brittanica)

This is why it’s no exaggeration when we say the stakes of the 2026 elections are enormously high. While Republican leaders signal their intention to cut benefits without offering any legislation, Democrats have actually introduced several bills to strengthen Social Security – largely by demanding that the wealthy begin contributing their fair share. Legislation introduced by Senators Sanders, Warren, and Whitehouse (along with Reps. Boyle, Hoyle, and Larson in the U.S. House) would extend the life of the trust fund for decades — without cutting benefits.

No doubt, voters have a lot to navigate heading into the 2026 midterms. Issues like affordability, health care, and Trump’s military misadventures are competing for attention. “We hope that our new public education campaign will remind voters that their earned benefits are on the line this year,” says CEO Max Ricthman. “They worked hard and contributed to Social Security with every paycheck and have very right to expect their benefits in full. We must not allow lawmakers to break that promise.”

Our political action committee has already begun endorsing Senate candidates in key battleground races who champion Social Security, such as Jon Ossoff (D-GA), Roy Cooper (D-NC), and Chris Pappas (D-NH). On the House side, we are supporting (among others) Christina Bohannon (IA-01), Rebecca Cooke (WI-03), and Paige Cognetti (PA-08).

While their opponents are promoting ideas that would put Social Security at risk, these candidates have distinguished themselves as advocates for today’s seniors and future beneficiaries.

This is not a one-off messaging opportunity or a single ad buy. As the election season unfolds, we will continue rolling out new content, resources, and organizing opportunities so that voters can stay informed and engaged right up to Election Day.

**********************

Watch our documentary about the history of Social Security, including the 1983 reforms here.

Read our Social Security is on the Ballot press release here.

Read about the campaign in 401K Specialist here.

- Published On: June 12th, 2026Categories: Congress, Democrats, Republicans

If Social Security Commissioner (and CEO of the IRS) Frank Bisignano brought anything with him from the corporate world, it is his ability to sell, sell, sell. At a June 10th hearing on Capitol Hill, the former Wall Street executive did his best to sell the fiction that EVERYTHING IS JUST GREAT at the Social Security Administration – despite massive understaffing, poor morale, and outright abuse of beneficiaries’ personal data.

While House Ways and Means Committee Republicans responded to Bisignano’s testimony with complete credulity, Democrats and Social Security advocates would have appreciated — pardon the pun — a little more Frankness. And maybe even a smidge of humility.

Bisignano bragged in Trumpian fashion about “the best all-around performance ever at the Social Security Administration” and tossed around business buzzwords like “best in class” as if SSA were an airline instead of a public agency serving some 330 million Americans. He declared that the “American people are winning” because of SSA’s performance. He should have added, “So much winning.”

“The American people’s experiences are very different from what the Commissioner is reporting,” said NCPSSM senior Social Security expert Maria Freese on this week’s edition of Capital Quick Takes. “The reality is not as rosy as they claim.”

2025 protest against Trump/DOGE cutbacks at Social Security field office in Evanston, IL (Matthew Eadie, Evanston Now)

Rep. Danny Davis (D-IL), the ranking Democrat on the House Work and Welfare Subcommittee, said Bisignano’s boasts of superior customer service do not align with what the congressman is hearing from his constituents in Illinois, who have complained of long waits at field offices, trouble making appointments, and problems getting help on the agency’s 1-800 number. “People across the country report waiting in long lines at Social Security offices or being turned away and told to make appointments, only to discover no appointments are available,” Davis said.

Commonsense alone would suggest that you cannot cut some 8,000 jobs at agency that was already at historic staffing lows (at a time when its customer base is rapidly growing), creating an enormous ‘brain drain’ of experienced employees who know how Social Security works… and expect that customer service would actually improve.

Kathleen Romig of the Center on Budget and Policy Priorities has done excellent work debunking SSA’s claims of ‘great success’ in serving customers.

“The loss of thousands of employees hit key customer service positions hard, including 3,800 staff who assist visitors at SSA field offices and callers to SSA’s national 800 number. SSA leadership responded by shifting thousands of remaining workers to new roles (with minimal training). But redistributing the too-few remaining workers to roles where they have little experience risks ameliorating one service delivery problem by exacerbating others.” – Kathleen Romig, Center on Budget and Policy Priorities

Under Bisignano, SSA has publicly released ‘data’ that purports to prove that customer service is “the best ever.” The data is a little fuzzy, to say the least. SSA claims to have reduced wait times on its 1-800 phone lines. What they don’t say is that they consider a call to have been completed and the wait time over when an AI bot answers or when a customer requests a callback. That doesn’t mean the callers’ question has been answered or their issue resolved.

“They fudge the numbers to get to some of these statistical claims,” says Freese, including the ludicrous claim that SSA has achieved an 80% drop in customer wait times!

CBPP’s Kathleen Romig has thoroughly debunked SSA’s claims of reduced wait times

Here’s a quick list of some of the misleading statements (if not outright falsehoods) that Bisignano peddled at the congressional hearing:

“I inherited a mess from the Biden administration.” WRONG! Under former Commissioner Martin O’Malley, customer service was actually improving despite chronic underfunding fron Congress.“We didn’t close down any field offices.” MISLEADING! In April, Business Insider reported that the Trump administration had at least temporarily closed in person services at more than a dozen field offices around the country, some for lack of resources due to DOGE cutbacks.

“We didn’t shut down anything facing clients.” MISLEADING! While no customer-facing service has been permanently ‘shut down,’ SSA wants to cut back in-person service at field offices by 50%, forcing seniors and people with disabilities to seek on-line help. SSA also kept revising its phone service policies to limit the kinds of assistance customers could receive on the 1-800 number, forcing people online instead. Not every senior or person with disabilities has the technical resources to conduct all of their business online.“We are relentlessly fighting waste, fraud, and abuse.” MISLEADING! Actual Social Security fraud is exceedingly rare. Before the Trump administration took over, SSA was one of the most efficient federal agencies, with an overhead rate of less than 1%. But the Trump regime (beginning with Elon Musk and DOGE) used the excuse of hunting for waste and fraud to decimate the agency.The real “abuse,” of course, is the administration’s misuse of Americans’ personal Social Security data for craven political purposes. The latest outrage was a whistleblower report that SSA planned to move 2.7 million living individuals onto the agency’s Death Master File as part of Trump’s war on immigrants. Our CEO called it “illegal and dangerous.” Bisignano glibly dismissed the report at this week’s hearing.

Two things are clear at this point: 1) Bisignano and his SSA will not truly be held accountable or expected to be straightforward until – and if – Congress changes hands next January and Democrats gain the power to do real oversight; (2) In the meantime, Bisignano will continue to try to convert SSA into a tech company instead of the sacred public trust it is meant to be.

****************************************************************************************

Post-Script

In his second role – CEO of the IRS – Commissioner Bisignano signed off on Trump’s $1.8 billion slush fund last month. Today, a federal judge indefinitely barred the Trump administration from moving forward with the fund, which was created for the bogus purpose of compensating people claiming they were “persecuted” by the government, including convicted January 6th insurrectionists.

READ our CEO’s written testimony for the 7/10/26 hearing here.

WATCH Capital Quick Takes with our senior Social Security expert Maria Freese here.

“I inherited a mess from the Biden administration.” WRONG! Under former

“I inherited a mess from the Biden administration.” WRONG! Under former