- Published On: July 30th, 2026Categories: Joe Biden, Medicaid, Medicare, President Trump, Republicans

President Lyndon B. Johnson signed Medicare and Medicaid into law 61 years ago today! These legacy Great Society programs could not be MORE IMPORTANT, but the political right has been targeting them for years. Now… Trump and congressional Republicans have chipped away at health coverage for seniors, people with disabilities, and lower income workers. We asked our legislative and policy director Dan Adcock to reflect on the history of both programs — and the threats they face today.

Q: Why was Medicare created in the first place?

A: Before Medicare was enacted, many seniors did not have health coverage. Insurance companies weren’t exactly eager to enroll older people. So the Congress and President Johsnon saw the need to create a federal health care program for the elderly. And that’s how we got Medicare in 1965.

Q: So was it a huge legislative accomplishment back then?

A: Yes, it was huge. Earlier, during President Truman’s time in office, he tried to create a national health care system. And that failed politically. But President Johnson picked up where Truman left off, because of the overwhelming need to provide health care to older people since the private sector wasn’t willing to do that.

Q: And that’s why he invited Truman to the White House for the signing of the Medicare law?

A: Yes. He invited Truman to the bill signing because LBJ was able to fulfill at least some of Truman’s vision.

Q: Why do we celebrate the enactment of Medicare today?

A: Because it provides every older American with essential health care coverage. And it’s been a great success story. Medicare is America’s most efficient health insurance system, covering some 72 million people while maintaining incredibly low overhead costs (except for the for-profit Medicare Advantage program, which we’ll get to later). All the polling about Medicare indicates that huge majorities of the public approve of it. Medicare is overwhelmingly popular regardless of party affiliation and age. And likewise, proposals to cut the program are equally unpopular.

Q: Why did they create Medicaid simultaneously as a sister program to Medicare?

A: Just as older people had trouble procuring health insurance before 1965, lower income Americans couldn’t afford to buy medical coverage at any age. So that was the reason that Medicaid was created. And then also the fact that, before Medicaid was enacted, the federal government did not help to finance long-term care, which has become enormously important as people tend to be living longer. And now, eligible beneficiaries can receive long-term care in skilled nursing facilities covered by Medicaid — and sometimes in the comfort of their own homes through Medicaid Home and Community-Based Services (HCBS).

Q: Some people get confused and think Medicare covers long-term care.

A: No, only Medicaid covers long-term care. But… if you’re admitted to a hospital for three days and need rehab or convalescence care, Medicare will cover it for up to 100 days. And if you still need that level of care after 100 days, you have to pay out of pocket or enroll in Medicaid.

Q: The Medicare Part A hospital trust fund is projected to become depleted in the early 2030s. What can we do to restore it to fiscal health?

A: Yes, we know from the most recent Medicare trustees report that the Part A trust fund reserves will run out in 2033, unless Congress takes action. At that point, there still will be money coming into Medicare in the form of payroll taxes – and 89% of benefits still could be paid. We don’t know for sure what that would look like, because it’s never happened before. But it would mean that payments to providers (doctors and hospitals) would be cut by 11%. So that’s why Congress needs to intervene and bring more revenue into the program.

Q: How big a threat to traditional Medicare is the privatized Medicare Advantage program right now?

A: Medicare Advantage was created based on the argument that private insurers could cover beneficiaries at a reduced cost to the federal government. But, unfortunately, it costs more to insure seniors through Medicare Advantage than it does through the traditional Medicare program. Not only are taxpayers picking up the tab, but traditional Medicare beneficiaries are basically subsidizing Medicare Advantage through higher monthly premiums.

Medicare Advantage is now capturing a growing share of the market, largely thanks to billions of dollars in (often deceptive or misleading) advertising by the insurance industry. If enough people join Medicare Advantage over traditional Medicare, that could result in a death spiral where it just becomes too expensive to run traditional Medicare anymore. And then Medicare Advantage – with all of its built-in disadvantages – would become your only option.

Q: What are our political concerns about Medicare with Trump in the White House and the Republicans still in the majority on Capitol Hill?

A: President Trump himself said the federal government can’t afford Medicare (and Medicaid) because of the need for ‘military protection.’ It’s absurd to tell seniors and lower income Americans that their federal health coverage must be cut because of Trump’s war in Iran. We won’t get into the politics of the war here. But we must honor our commitment to provide basic health care to the most vulnerable among us – like every other industrialized nation does.

Let’s not forget about Trump’s Big, Ugly Bill, which cut nearly $1 trillion from Medicaid. That not only hurts lower income Americans who need that coverage, but it affects seniors who are dually eligible for Medicare and Medicaid — not to mention the millions of elderly who receive long-term care through the Medicaid program. The full impact of those cuts hasn’t even been felt yet, because the most harmful provisions of the Big, Ugly Bill don’t take effect until 2027.

Q: To wrap things up here, what would you tell people who are concerned about the future of Medicare (and Medicaid)?

A: Let your members of Congress know that you don’t want to see Medicare and Medicaid further cut or undermined. And equally importantly, vote for candidates this fall who understand that, 61 years ago, this country made a commitment to seniors and lower-income people that they would no longer have to live without basic health coverage. We encourage voters to support candidates who will protect seniors and working people in the next Congress. Depending on the result of the next two elections, maybe we can turn this around and undo the damage that Trump and his party have inflicted on these crucial programs.

***************************

Read our CEO’s op-ed in Common Dreams, entitled “Celebrate Medicare & Medicaid – and Protect them from Trump.”

Listen to our podcast episode, “Keep AI Bots Out of Medicare!”

- Published On: July 23rd, 2026Categories: fiscal commission, seniors, Social Security

Soon-to-be retired Senator Dick Durbin’s (D-IL) new PROMISE Act is the latest in a wave of proposals to establish a ‘fiscal commission’ to address Social Security’s looming financial shortfall, instead of allowing Congress to do its job and devise its own proposals.

Durbin’s bill would authorize the four-person Social Security Advisory Board to draft a 50‑year solvency bill that would be fast‑tracked through Congress by the end of the current legislative session. While it differs from earlier commission proposals, Durbin’s legislation still relies on an outside body to formulate changes to a program that 70 million Americans rely on for basic financial security.

On the latest episode of our Capital Quick Takes video series, communications director Walter Gottlieb interviews our President and CEO Max Richtman about Durbin’s bill and other efforts to create fiscal commissions for Social Security.

WALTER: Senator Durbin and several cosponsors have a bill to create a ‘fiscal commission’ to address Social Security’s solvency problem. We don’t love the idea because it punts the ball over to an outside panel to propose solutions for Social Security – instead of just letting Congress come up with ideas on its own and act. Is that about right?

MAX: These commissions are kind of a legislative approach to avoiding responsibility and accountability. Just to be clear, I have great respect and admiration for Senator Durbin. He has been a longtime champion of Social Security, Medicare, the Older Americans Act, and all of the programs older Americans rely on. I commend him for that.

That said, I have serious concerns about his proposal for a commission that could push through major changes to Social Security in the final days of this Congress. It would likely occur during a lame-duck session, after the election, when many members are on their way out. Those members could be asked to vote on sweeping changes to Americans’ earned benefits, when they’ll no longer be accountable because they’re leaving office. I think that’s a real problem. And I think members of Congress should be 100% responsible for any changes to the Social Security program.

WALTER: Many of the Fiscal Commission proposals we’ve seen would bypass ‘regular order’ in Congress, meaning that any changes could be fast-tracked to a floor vote before the public or advocates have adequate time to respond.

MAX: That’s exactly right. All these commissions have expedited procedures that do not go through regular order. You know, Social Security is such an important program to everybody, not just seniors, but working people who need these benefits when they retire, who have coverage for life and disability insurance. It’s so important.

Why not allow members to introduce bills? Hold hearings in committees of jurisdiction? Allow advocates like ourselves testify on proposals? Have legislation that’s voted on, debated and voted on? That’s the way these changes should be made.

WALTER: And just to be clear, we favor revenue-side solutions that would bring more money into Social Security.

MAX: Yes, we support legislation that demands the wealthy begin paying their fair share into Social Security by scrapping the payroll wage cap. The last time Social Security was ‘reformed,’ in 1983, about 90% of wages were subject to the payroll tax. Now, because of rising income inequality, only about 80% of wages are covered. So adjusting the cap is only fair.

On the other hand, we reject proposals that would cut benefits, including raising the retirement age, means-testing or ‘capping’ benefits, or adopting a more miserly formula for cost-of-living adjustments (COLAs). Seniors should not be asked to bear the burden of strengthening Social Security’s finances. Unfortunately, benefits could be cut more easily through a commission process where individual members of Congress have less accountability.

WALTER: You worked on Capitol Hill for a long time. Fiscal commissions don’t have a stellar track record, right? In 1983, there was the Greenspan Commission, and in the 2000s we had the Simpson-Bowles Commission.

MAX: Well, they’re different. The Simpson-Bowles Commission collapsed. They didn’t have the votes to even get a recommendation to Congress, unlike the Greenspan Commission, which produced a proposal for Congress to consider. Back in 1983, Social Security was only months away from being unable to pay full benefits. The commission helped develop a plan that extended solvency well beyond that immediate crisis. But its proposals still had to go through Congress, which embellished and changed the Greenspan Commission proposal quite extensively.

WALTER: If the Greenspan Commission actually came through with a proposal that was embellished and acted on, why don’t we want another Greenspan-style Commission today?

MAX: Because unlike the current commission proposals, the Greenspan panel’s recommendations were not fast-tracked through Congress. After the commission issued its proposals, Congress held public hearings – and lawmakers actively debated and amended the legislation in both the House and Senate Committees of jurisdiction before it was signed into law.

That is not how Durbin’s commission idea would work, nor any of the similar proposals we’ve seen on Capitol Hill in recent years. Creating a fiscal commission now would set the stage for members of Congress to avoid responsibility. That isn’t right, because it’s their job to step forward and strengthen Social Security without relying on a commission for political cover. We need to make sure they do that.

WALTER: So, these commission proposals would give individual members of Congress political cover to do something deeply unpopular, like cutting benefits?

MAX: Absolutely. And I’d like to note, since this is an election year, that a candidate simply saying, “I support Social Security” isn’t good enough. Candidates need to say where they stand on improving the program for the long term. Do they support bringing in more revenue in a fair, equitable way, or do they support cutting benefits — which I don’t believe most Americans would accept.

Looking Ahead

The National Committee is joining other prominent seniors’ advocates — including AARP — in opposing the latest fiscal commission proposal. Social Security reforms must be made transparently through standard Congressional processes, with ample time for public scrutiny and debate. Any legislative effort to address the program’s long‑term challenges should start from a simple principle: benefits must be protected and strengthened, not cut — and older Americans, people with disabilities, and survivors deserve a real voice in shaping Social Security’s future.

******************

Watch the full conversation with Walter and Max on Capital Quick Takes here.

- Published On: July 22nd, 2026Categories: Centers for Medicare and Medicaid Services, healthcare, Medicaid, Medicare, Trump Administration

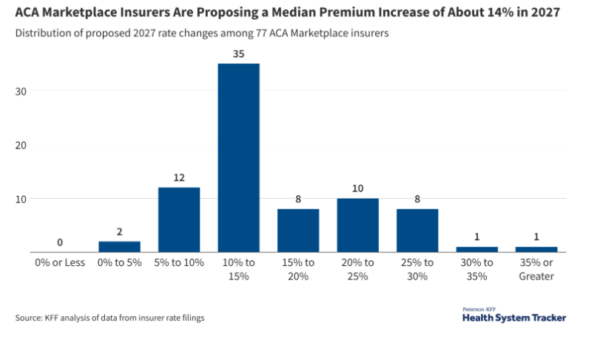

New reporting shows Affordable Care Act (ACA) premiums are set to spike by an average of 14% in 2027, on top of last year’s double‑digit hike. It’s exactly what you’d expect from a Trump administration that has made life more expensive and health care less secure for the most vulnerable Americans.

For millions of Americans who buy coverage on the ACA marketplaces, the story of the past two years is simple: the bill got bigger, the help got smaller, and people are walking away from coverage. As our health policy expert Anne Montgomery, puts it:

“For modest working‑ and middle‑class people — especially those ages 50 to 64 — premiums are jumping far more than 14%. It’s pure sticker shock. If the policy suddenly costs you that much more, many people simply cannot swing it and decide not to buy or continue coverage.” – Anne Montgomery, NCPSSM

The latest premium spikes are not a fundamental flaw of the ACA; they are a direct consequence of reckless policies in today’s Washington. Congressional Republicans purposely let enhanced ACA tax credits expire – making coverage more expensive. Those temporary subsidies, originally expanded during the pandemic, were designed to make premiums affordable for low‑ and middle‑income households.

When the subsidies disappeared, the monthly amount people had to pay out of pocket jumped — for some people by 100, 200, or even 300%. No wonder ACA enrollment has tanked. Thanks to GOP hostility to the ACA, millions of Americans could no longer afford it.

While Trump’s party refused to extend ACA tax credits, his misguided tariffs and the deeply unpopular war in Iran has raised the cost of essential medical goods and prescription drugs. In response, insurers are passing these escalated costs along — in the form of higher premiums and cost‑sharing.

Trump’s Big, Ugly Bill – which slashed nearly $1 trillion from Medicaid — has only exacerbated the problem. The Kaiser Family Foundation reports that some 3.8 million people have lost Medicaid coverage since the bill passed in 2025. For someone who loses Medicaid, an ACA marketplace plan at today’s prices may not be a realistic option.

Getty Images

By definition, Medicaid beneficiaries are low‑income; if they are pushed off the program and told to “go to the exchange,” they will find premiums far beyond reach. On the flip side, people who drop their ACA coverage due to soaring premiums may try to fall back on Medicaid, only to run into reduced funding and bureaucratic obstacles designed to keep them out. Many will end up in the worst of all worlds: uninsured.

Instead of trying to mitigate these health coverage losses, the President and his allies in the GOP‑controlled Congress are escalating their crusade against Medicaid. HHS Secretary Robert F. Kennedy Jr. and CMS Administrator Mehmet Oz have announced they are cutting off more than $1 billion in Medicaid funding to California and Minnesota, citing “suspected fraud,” without providing concrete evidence. It’s the latest in a series of punitive actions aimed at Blue states, and it threatens the health and well-being of some of our most vulnerable citizens.

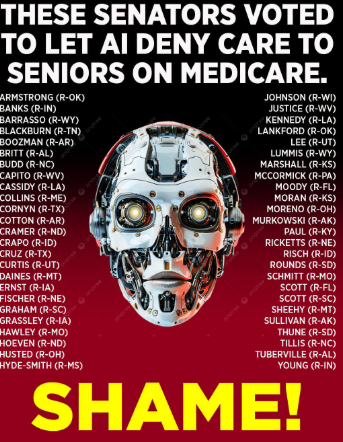

At the same time, Senate Republicans recently voted down a Democratic bill that would have outlawed the use of AI for prior authorization decisions in Medicare. This means that enrollees will continue to have robotic, AI entities make life-or-death coverage determinations.

Source: Social Security Works

The good news is that the primary fix for the ACA affordability crisis is both clear and achievable. The next Congress could restore and expand the premium tax credits that have expired. This “absolutely would” translate into lower costs for consumers and bring many people back into the marketplace, according to our health policy expert, Anne Montgomery.

Restoring subsidies to the levels we saw a few years ago would make plans affordable again for working‑ and middle‑class families who have been forced to drop coverage. There is, “really [no] other fix” that can match that impact in the near term,” says Montgomery.

That’s the choice facing lawmakers. They can stay on Trump’s course, which prioritizes insurance company profits and tax cuts for the wealthy and large corporations — or they can change direction. November’s midterm elections will be a crucial fork in the road.

************

Listen to our podcast on the dangers of AI in Medicare prior auth HERE

- Published On: July 14th, 2026Categories: ageism, Equal Time, Medicare, Social Security

In his latest column for The Atlantic titled “An Oligarchy of Old People,” author Idrees Kahloon correctly identifies a troubling symptom of the 21st century economy — a younger generation left worse off than those who came before them — while misdiagnosing the cause.

Rather than identifying the true culprit, namely wealth inequality and the concentration of power at the very top of the economic food chain, the article shifts blame to older Americans as some sort of monolithic class, regardless of income. This kind of scapegoating is exactly what (middle-aged!) finance and tech oligarchs like Thiel, Musk, Zuckerberg, and other billionaires want.

In fact, that same group has repeatedly sought to sow division and redirect blame for income inequality toward immigrants, minorities, and now older Americans. Kahloon plays into that narrative by framing the problem as “Boomers vs. everyone else,” rather than “the wealthy elite vs. everyone else,” needlessly pitting generations against each other.

Many in the media are trying to pit the generations against each other

The simple facts are that older people of varying income levels generally have a higher net worth and more assets than their younger counterparts. This is a normal feature of a functioning economy.

Ultimately, what we have seen over the last 50 years is a consistent decline in wealth equality and workers’ rights across the board. The built-in disparity between young and old has not been created by Social Security and Medicare; rather, it has grown because of broader structural forces (which we will get into later).

Now, let’s take a look at some of Kahloon’s claims, particularly those that touch on Social Security and Medicare.

“In 1965, Medicare was created. A major expansion of Social Security followed in 1972. These changes were remarkably effective: The share of elderly people living in poverty dropped by more than one-third within a decade. But because these programs are broad-based entitlements, they have transferred huge sums to the prosperous, too. The portfolios of that latter group, meanwhile, have been swelled by a rising stock market and rising home values, outcomes that may not be entirely replicable for younger generations. As a result of all of these factors, intergenerational inequality between old and young has not merely reversed. It has accelerated.”

Mr. Kahloon is correct that the changes made by FDR’s “New Deal” and LBJ’s “Great Society” were “remarkably effective” and remain so. In fact, Social Security and Medicare are the most successful anti-poverty programs in American history. But the article makes a huge leap in citing Social Security and Medicare as the main factors behind the rise in intergenerational inequality. The grounds for that causal claim are shaky at best.

LBJ signs Medicare and Medicaid into law in 1965

The real drivers of rising wealth concentration and intergenerational disparity (aka the oligarchs) are far more to blame than Americans’ earned benefits. The last several decades have seen:

- Decline of unions and labor’s bargaining power: Union coverage has fallen dramatically since the 1970s, weakening wage growth, reducing retirement benefits, and shifting power from workers to owners.

- Rising top incomes of “superstars,” finance, and executive pay: The share of income going to the top 1% and 0.1% has exploded, driven by finance, tech, and corporate governance changes that reward executives and shareholders far more than workers.

- Tax and transfer policy changes: Since the 1970s, effective tax rates on the very top earners fell substantially. For the top 0.01%, the effective federal tax rate dropped from about 59% in 1979 to 35% in 2004. Today, that number sits at a staggeringly low 24%. Meanwhile, middle-class and working-class families faced rising costs in every area of importance: Housing, education, and health care, with fewer public supports.

Social Security and Medicare have reduced old-age poverty and provided baseline income for seniors on fixed incomes. They are not the cause of rising wealth inequality, and without them, 40% of seniors would slip into poverty, while even more would lose their health care.

Taking a more cultural view, Kahloon opines that:

“Respect for elders is being replaced by resentment of elders. A majority of young Americans no longer believe in the American dream. Many Millennials and Gen Zers expressly blame the Boomers for that, accusing them of hoarding wealth, jobs, and power. Many of these accusations are inchoate, but they are not entirely baseless.”

These accusations are in fact, inchoate — and baseless, but Kahloon does nothing to correct that. Instead, it appears the author would rather further stoke these fears and divisions than place blame on the real culprits. Doing so might upset The Atlantic’s primary owners/investors — the Emerson Collective — a venture capital firm also known for its involvement in the AI, Crypto, and oil industries.

Blaming “Boomers” as a class allows the real architects of inequality (like the Emerson Collective) to avoid scrutiny. It lets them redirect anger from the concentration of wealth and power at the top to a generational fight between older and younger workers. No wonder ageism in this country remains rampant.

Finally, Kahloon suggests:

“An intergenerational recalibration can come about in gentler ways than Moyn’s: The wealthiest Social Security recipients, for instance, could forgo some of their scheduled benefits, which could instead be contributed annually to “baby bond” accounts for America’s children.”

This is a classic straw man that is nothing more than a call for means-testing Social Security benefits. As we’ve argued before, means-testing undermines the very nature of Social Security, which is social insurance, not welfare. It is designed to be universal, tied to work and contributions, and protected from the political whims that target traditional welfare programs.

It’s in the interest of America’s oligarchs to divide the generations

Once that dam breaks, Social Security will become like any other welfare program, subject to cuts whenever Republicans control Congress and the White House. To save significant money, means testing would have to cut deep into the heart of the middle class.

Slashing Social Security and Medicare to address wealth inequality would do nothing to address the core issues and causes of inequality. In fact, many conservatives want to slash the social safety net (See the massive cuts to Medicaid and food assistance in Trump’s Big, Ugly Bill), while stoking divisions among us. The real fight is not old vs. young. It is workers and families vs. financial elites that benefit from a K-shaped economy – and a distracted populace arguing over generational differences.

****************************

Listen to our podcast interview about ageism in America with expert S. Jay Olshansky here. - Published On: July 7th, 2026Categories: GOP, President Trump, privatization, Social Security

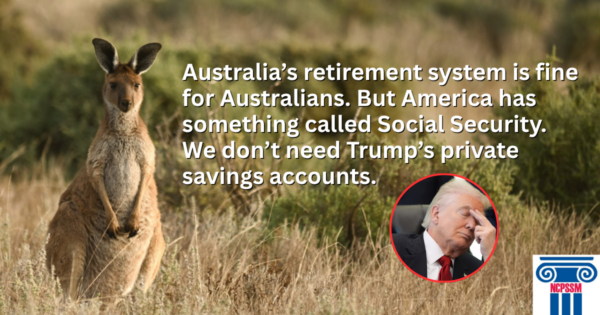

After turning the page on his self-indulgent USA250 bonanza, marred by extreme heat and disappointing attendance, President Trump has once again set his sights on Americans’ earned retirement benefits. On Monday, he announced that his administration is “working on a plan” to create accounts for adults loosely inspired by Australia’s retirement savings system – and similar to the Trump accounts for children.

Our president and CEO Max Richtman told MarketWatch today that Trump should be working on strengthening Social Security instead of “toying around” with federally-seeded private accounts.

“We would advise President Trump to focus on Social Security – a program that has worked splendidly for more than 90 years to provide Americans with basic retirement security” – Max Richtman, President and CEO, NCPSSM

Far from fortifying Social Security for the future, these private Trump accounts are a ‘back door way’ of privatizing Social Security. First, Treasury Secretary Bessent admitted as much; then, Senator Ted Cruz affirmed the “dirty little secret” of how these accounts will lead to privatization.

The push for Trump accounts is not coming from seniors’ advocates – or even from seniors themselves. Rather, it seems to be the brainchild of Bessent and Commerce Secretary Howard Lutnick. Fox Business News reports that these two cabinet members are fleshing out the private retirement plan proposal.

Uncoincidentally, Bessent and Lutnick are entangled with Wall Street. For them, a new “retirement account” system is a chance to expand the pool of money flowing into private investment products — and shift more retirement risk from the government to individuals.

This might make billionaires and Republican donors in the financial sector happy, but for the retirees who rely on Social Security for all or most of their income, the risk is simply too great to bear. In a privatized system, one bad year in the markets could lead to a 30% benefit decrease.

The Trump children’s accounts snuck through in the Big, Ugly Bill, whose main purpose was to slash social services while showering the wealthy with new tax breaks. Under the pilot program from the 2025 megabill, the federal government seeds each children’s account with $1,000. That money is then invested in a Wall Street fund, to which parents can also contribute. It’s a handy way to funnel taxpayer dollars to the financial markets, when private-sector savings plans for children (and adults, for that matter) already exist. Much like Trump Rx, the president has co-opted an extant private sector function and branded it as his own.

Now, Trump is recycling that branding for adults by piggy-backing off of Australia’s model – apparently without understanding the Australian model in the least. The key difference is that Australia’s plan is backed by mandated employer contributions rather than federal seed money. Australia’s retirement system, called superannuation, is built on a few simple principles:

*Employers must contribute 12% of an employee’s pay into a retirement account that the worker owns.

*Contributions go into a personal, market-invested account tied to the worker, not into a government pool.

*The system is designed to supplement Australia’s public pension, not replace it.

American employers (including many GOP donors) probably would not be thrilled to pay 12% of workers’ earnings into a new, Australian-style retirement system. U.S. employers already contribute 6.2% of wages to Social Security, matching their employees’ contributions. As Max Richtman points out, “Australia’s retirement system may be fine for Australians, but we already have a proven federal retirement program that deserves the President’s attention.” So here’s an idea: why don’t we stick with Social Security, which, with some common-sense improvements, can remain the sturdy financial lifeline that it has been for more than 90 years – instead of banking on yet another Trump branding scheme?

***************************************’

Watch our health policy expert Anne Montgomery’s takedown of Trump Rx HERE.

Read an article featuring our President & CEO’s thoughts HERE

Listen to our “You Earned This!” Podcast HERE